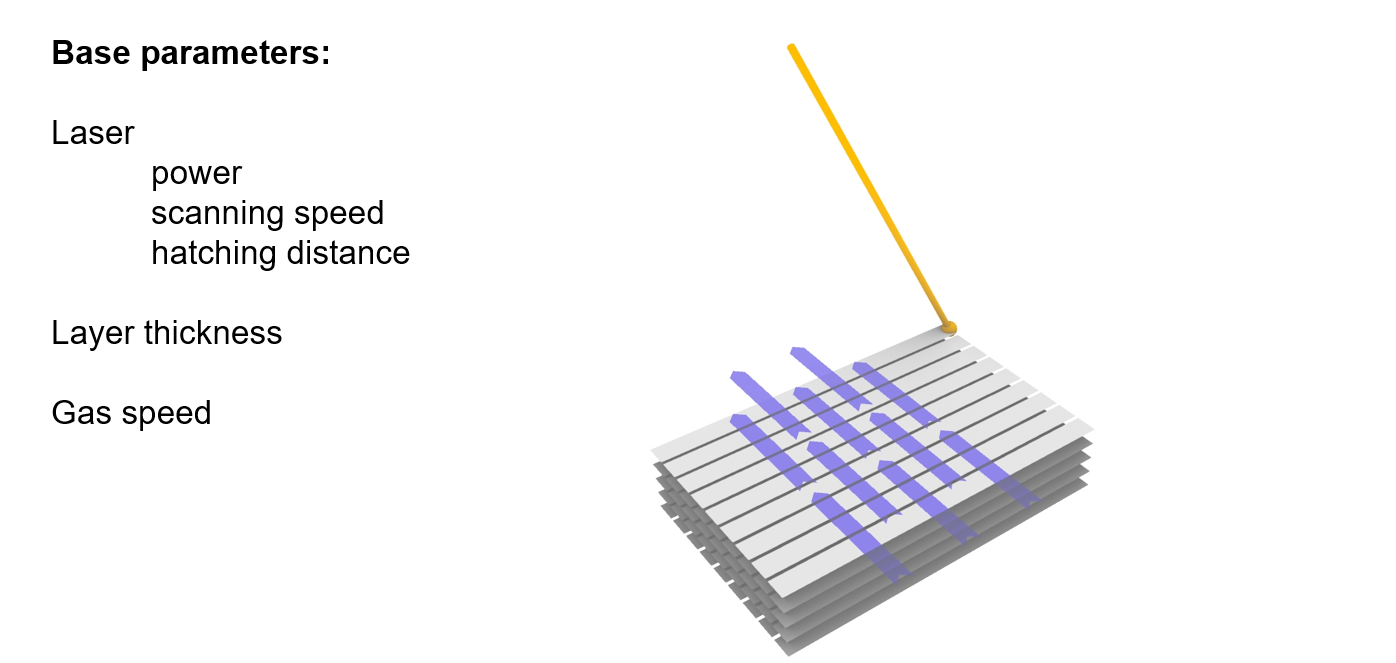

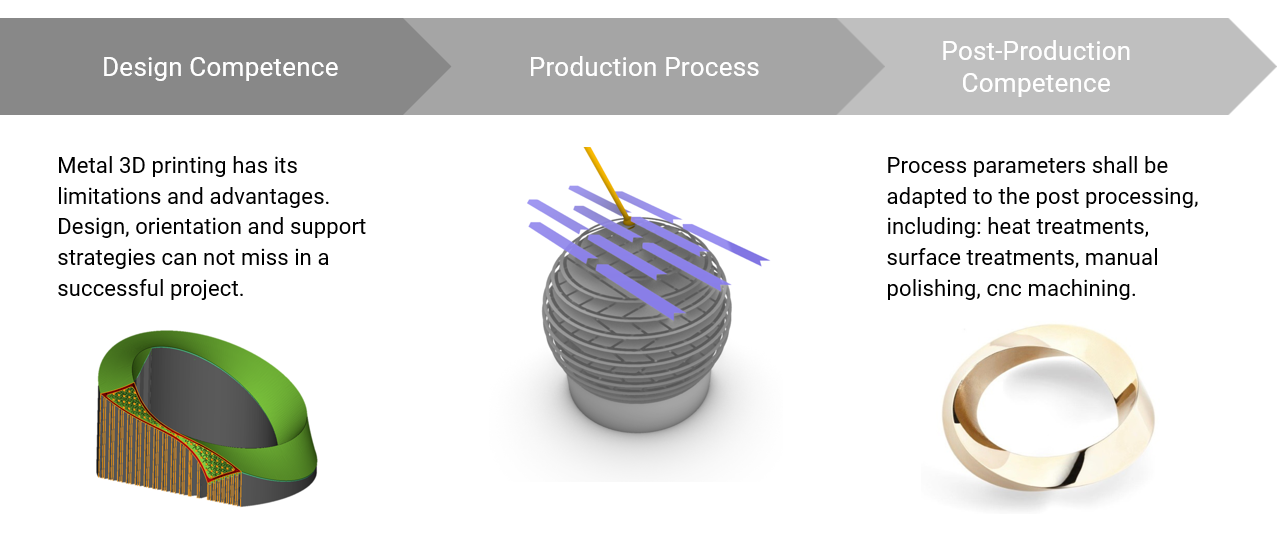

Geometry driven parameters and relevance of open material system for jewelry additive manufacturing.

a speech by Marco Giuseppe Andreetta

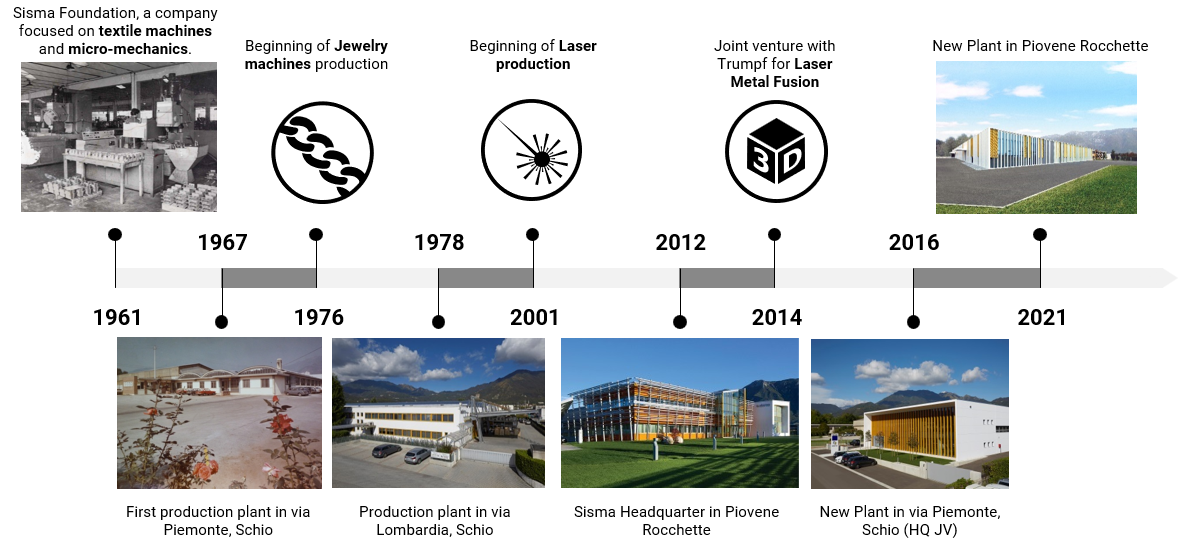

Sisma, a growth journey of more than sixty years

More than 40 years in jewellery making machines, more than 60 years in micromechanics

More than 20 years in laser manufacturing and laser based process expertise

More than 10 years in manufacturing of metal 3D printing machines designed for small and complex geometries

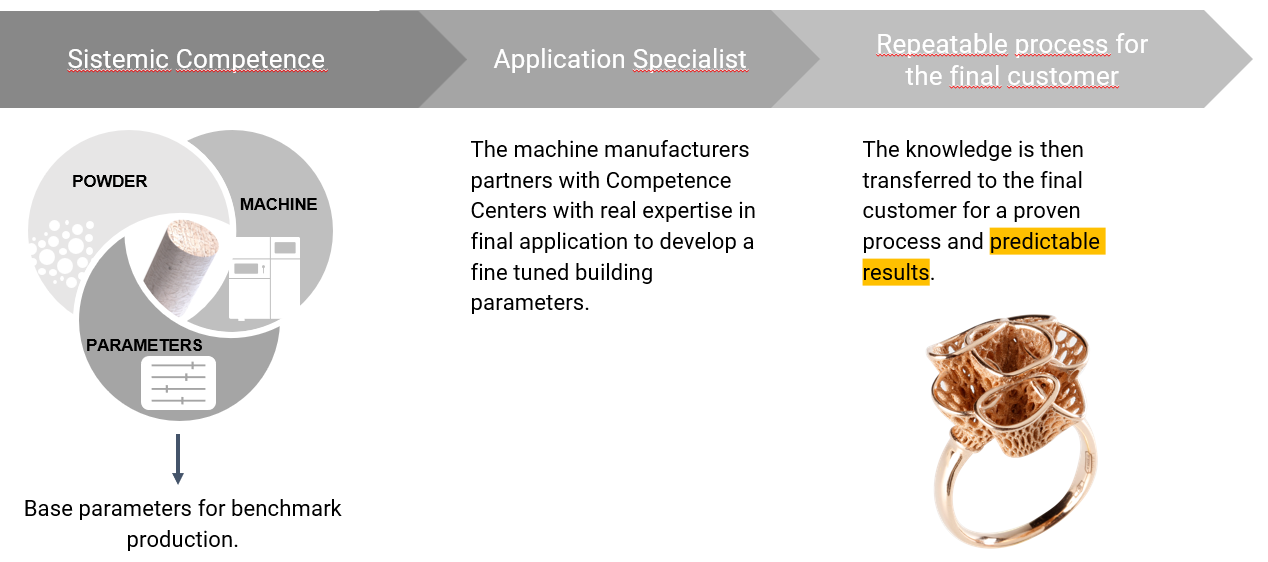

Open systems and relevance for jewellery additive manufacturing

Open systems are a value for the jewellery manufacturer, enabling:

freedom of choice

→ potentially every powder manufacturer could be validated

possibility to adapt the building parameters to each geometry

→ different geometries have different requirements. In order to exploit all the benefits of additive manufacturing it is necessary to fine tune the building strategy

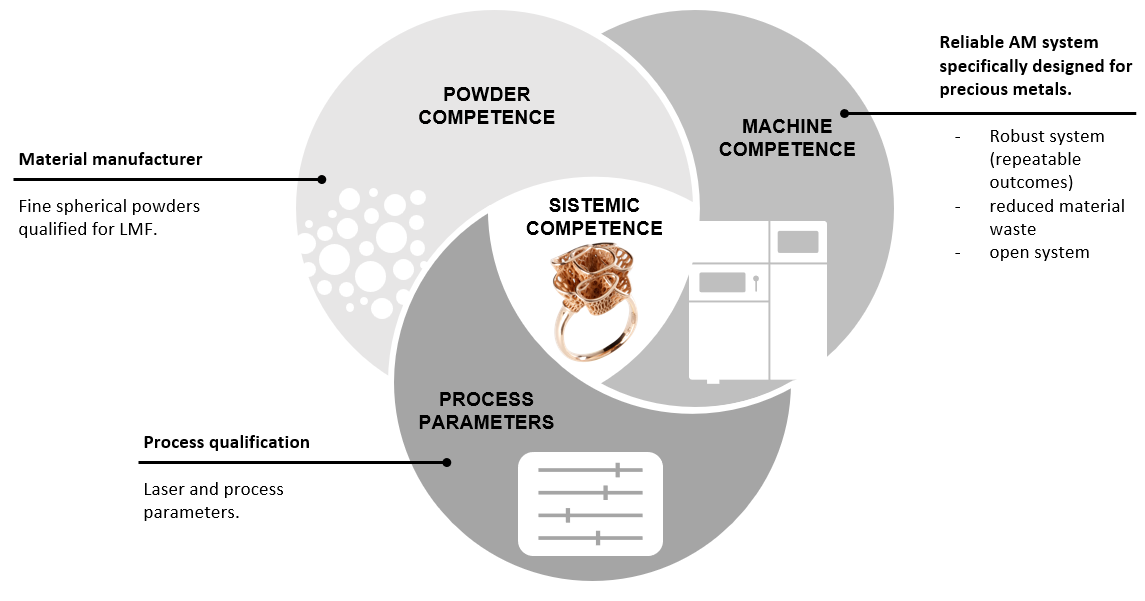

A harmonizedapproach to precious metal 3D printing

A harmonizedapproach to precious metal 3D printing:

to establish a SISTEMIC COMPENTENCE

– Density > 99,9%

– Digital microstructure

– Compliance with jewelleryqualitystandards

– Building strategiesadapted to the post processing

Compatibility with materialmanufacturers of precious metals

Having open parameters grants compatibility with multiple precious metal material supplier, leaving the customer free to evaluate existing suppliers or propose a new one for validation.

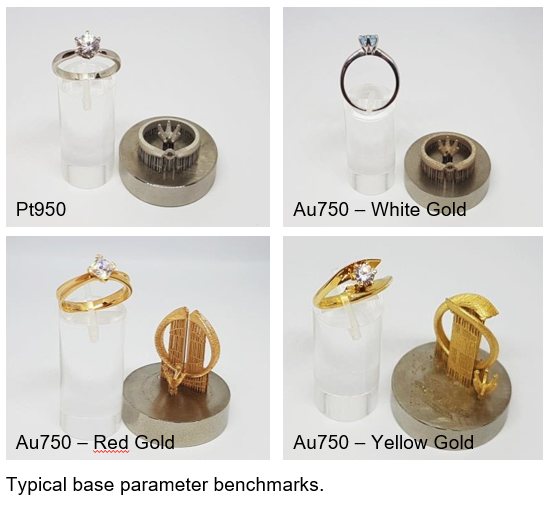

Currently available alloys for Jewelry additive manufacturing:

Preciousmetals:

Au750 White Gold

Au750 Yellow Gold

Au750 Red Gold

Ag925

Non preciousmetals:

Bronze9010

Stainless Steel

Titanium alloys

Partnership with Application Specialists:

The application specialist works alongside with the final customer with the machine manufacturer support.

We chose to partner with one application experts for each strategic jewellery market, in order to accomodate requests from all over the world.

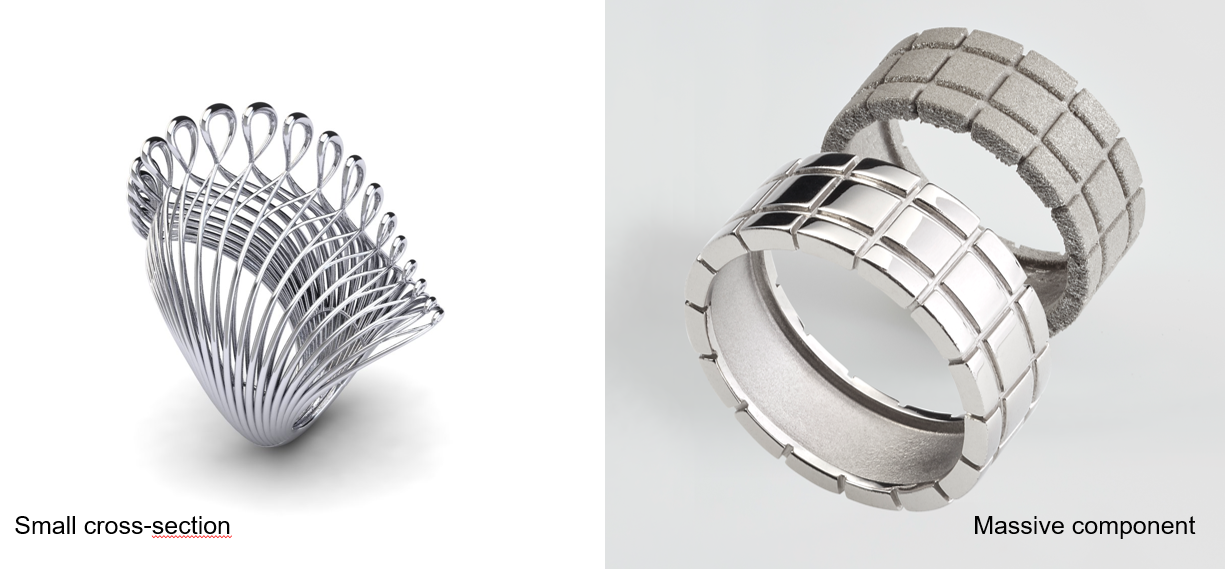

Material choice with smaller than usual grain size

Easy to remove support, only supportive function

Massive part

Part description: wall thickness changes across the part

Validationcriteria: mechanical properties, density and geometry compliance, build speed

Medium or variablebeam spot

Supports: heat exchange, supporting and anchoring function

Benefits from pre-heating

Skin/core laser parameters to increase build speed

Beam spot diameter: small beam spot for special applications

“Pixel” technical sample – Bronze 90-10

▪ No correlation with conventional technologies

▪ The part is made of interconnected pieces

▪ The complete part is made in a single Ø100mm print job

▪ Combination off additive manufacturing, polishing and surface treatment (gold plating)

▪ Small beam spot parameter choice (30µm) to make the geometry possible

▪ Parameter fine tuning of the beam compensation (on the file preparation) rather than tweaking the CAD geometry

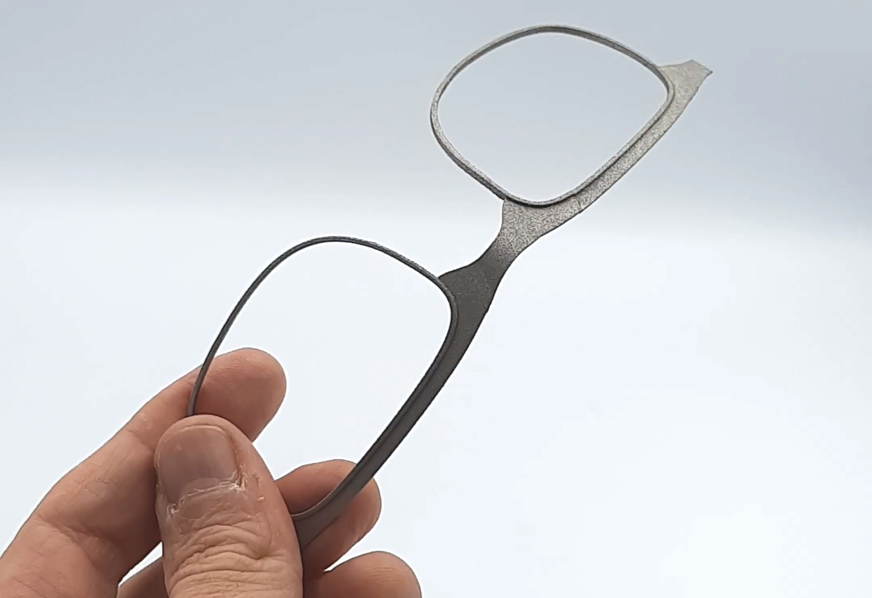

Titanium: a growing trend in jewellery

Titanium popularity is increasing in the jewellery market.

Once considered a minor metal relegated to aviation and medical industry, is now gaining importance for many reasons:

– weights a quarter of gold → bigger items are worn without discomfort

– anti-allergenic (e.g. in watchmaking Titanium can be used by whom is allergic to Nickel contained in 904L)

– can be processed to show a wide range of boldcolours

Titanium: traditionaltechnologiesdrawbacks

Titanium has its drawbacks for traditional machining:

Traditional processing of Titanium is costly.

Dedicated machinery is used to safely and effectively work with this alloy.

Machining Titanium usually requires:

– high torque machine and low speeds, to reduce the heat generation

– higher speeds usually generate unwanted hardening of the metal, increasing tool wear

Casting Titanium is a difficult task as well.

Titanium: advantages of 3D printing

Titanium can be 3D printed easily and safely on a well tuned machine.

Indeed, is one of the easiest material to be 3D printed:

– highly self supporting → a small amount of supports leads to increased geometry freedom and reduction of post processing

– relatively low elastic modulus → controlled distorsion during 3D printing

And, moreover, a wide range of alloys are already developed for other demanding markets.

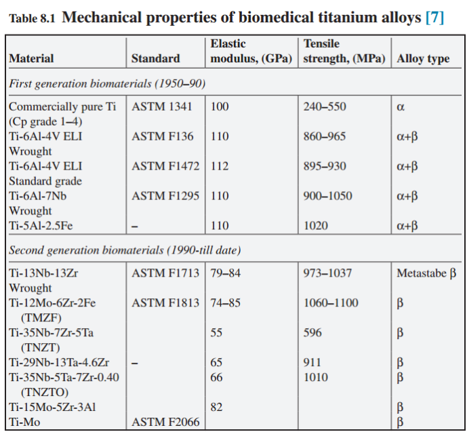

CommonlyAvailableTitaniumalloys

Ti6Al4V – gr.23 ELI

Industry standard for aerospace and medical applications. More than 350 HV5

Ti gr.1, Ti gr.2

This two Titanium grades shares corrosion resistance, weldability, and high ductility. Almost pure Titanium, other elements are less than 0,2%. Roughly 225 HV5

Ti6Al4V – gr.5

Widely available on the market, it shares the chemical composition of gr.23 but with higher amount of Oxygen.

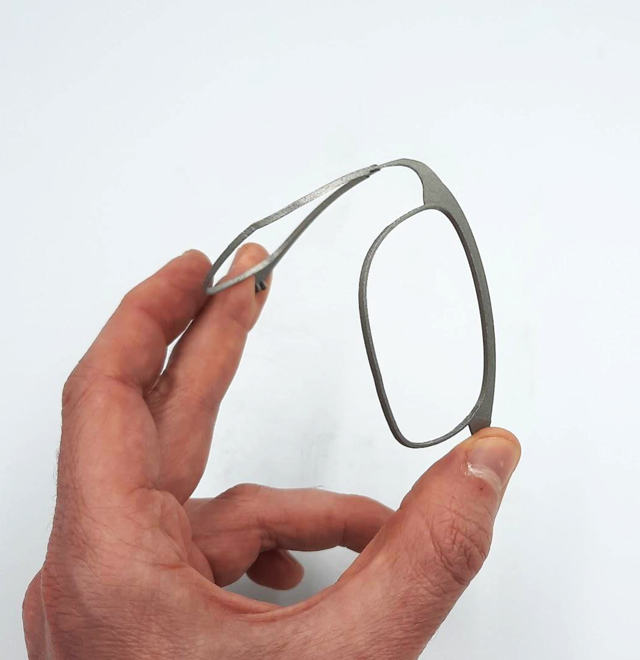

Serial production of hollow Titanium chain. Titanium itself helps stacking easily complex geometry with small amout of supports.

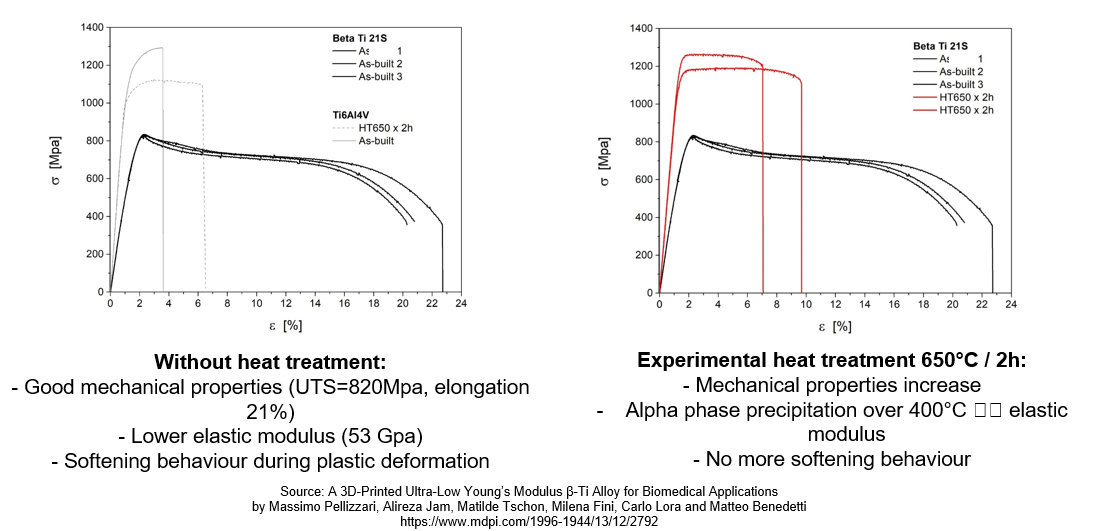

Source: A 3D-Printed Ultra-Low Young’s Modulus β-Ti Alloy for Biomedical Applications by Massimo Pellizzari, Alireza Jam, Matilde Tschon, Milena Fini, Carlo Lora and Matteo Benedetti https://www.mdpi.com/1996-1944/13/12/2792

New Titaniumalloybeingresearched

Requirements:

Lower elastic modulus

Great fatigue resistance

Optimal corrosion resistance

Optimal biocompatibility (alloy without Vanadium)

New Titaniumalloybeingresearched

Findings:

Lower elastic modulus was also useful to control the deformations during the printing process

–> the new material has even higher buildability characteristics if compared with conventional Ti6Al4V

It may be possible to completely avoid the heat treatment or at least switch to a lower temperature aging and stress relieving process

–> Possibility of using cheaper furnaces and avoid vacuum heat treatment for Titanium

New Titaniumalloybeingresearched

FlexibleTitaniumapplications in the luxury market

Currentdevelopments in Sisma :

Development of new alloys

Fine tuning of existing alloys for the LMF process

Fine tuning of the whole process (powders, LMF, heat treatment, inert gas mixture choice) to satisfy specific market requests.

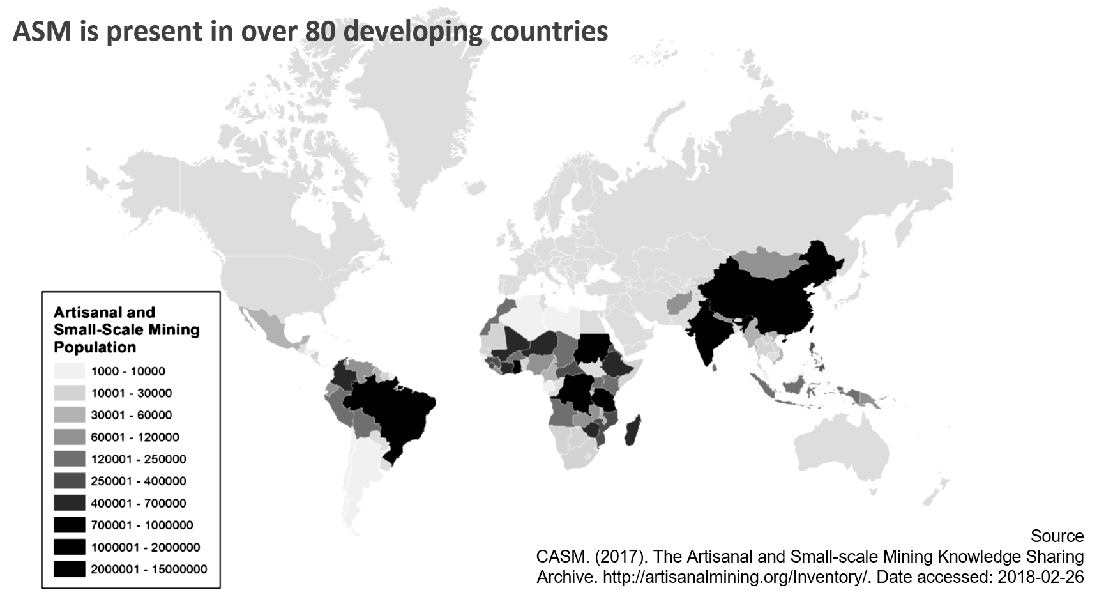

The power of gold industry to generate positive social and environmental impact in mineral supply chain

a speech by Marco Marcin Piersiak

Abstarct

CSR. Sustainability. Responsible sourcing. Conflict free. These are key words that have become increasingly important in the gold industry in recent years. Awareness on the issues in gold mining, such as the financing of conflict, human rights abuses, unsafe labor conditions, environmental destruction and negative social impacts, has increased. This requires the industry to take a closer look at its gold supply chains and promote solutions that provide access to conflict-free, legal or responsible gold in order to minimize the reputational risks for the sector. Additionally, consumers are increasingly concerned about the origin of the products they buy and demand improved conditions throughout the supply chain of consumer goods. This is being reflected in the consumer spending on ethical, responsible or green products which have been increasing steadily. Market studies show that ethical consumerism is growing significantly, and ethical brand values drive purchase decisions. Responsible gold sourcing therefore is not only a business opportunity and strategy for businesses worldwide, but a “must” for those companies who want to stay relevant for future generations. Companies that provide their clients with responsible gold products can position and distinguish themselves from others and provide consumers with a more meaningful brand experience, while improving their corporate social responsibility and contributing to the Sustainable Development Goals.

Alliance for responsible mining: Who we are?

Non-Profit Organization established in 2004

Leading global expert on gold artisanal and small-scale mining (ASM)

Experience with 150 mines in 24 countries

GOLD AND PRECIOUS METALS MINING

What about recycled gold?

90% of the work force in mining

10% of global gold production

20 million people

A sector with challenges, but…

Mining generally has a poor reputation, and in particular artisanal mining is often associated with:

– Illegality and informality or the funding of armed conflicts

In Honduras, it is estimated that there are 2.500 informal artisanal miners, informal = don’t comply with all mining norms.(legal and economical barriers to the formalization)

– Artisanal miners often live in precarious conditions, there is poor health and safety of workers, and in the worst cases you can find child labor, accidents and deaths.

– Also, gender equality or discrimination may be common.

– ASM is one of the principal sources of mercury pollution and intoxication and you may have seen pictures of vast environmental destruction due to unorganized, illegal mining.

In Honduras : ASM mining communities use approx. 90 T of mercury / year.

Why are all of these issues so prevalent in the ASM sector?

– Lack the enabling environment to improve their conditions: ASM often isn’t supported by the state but may be ignored, stigmatized or even persecuted

– Where mining legislation does exist its often not applicable or approriate to ASM, forcing these organizations to comply with regulations meant for large scale mining, only adding more barriers for inclusion.

– Often located in remote and unregulated áreas where the state isn’t present and regulation is taken over by locals or other groups

– They also lack access to necessary resources to perform mining in an organized, efficient manner:

– absence of education and training to formalize.

– zero access to formal banking or finance to develop their activity

– Lack of access to efficient and environmentally friendly tools and technology

Despite all these challenges this sector has incredible potential to contribute to local & national development. In Honduras, mining sector 100 and 150 USD Million of dollar every year. And the ASM sector has a great role to play in this aspect an. ASM is a source of income for many families

Why engage with ASM?

Risks & Reputation

▪ Risks of not engaging.

▪ Excluding the sector doesn’t contribute to solving its problems but deteriorates the reputation of the sector as a whole.

Corporate Social Responsibility

▪ The biggest positive economic, social and environmental impact to be made in the gold industry is in ASM.

A holistic sourcing policy should be inclusive of gold from artisanal and small-scale mining.

Mining won’t stop

Phaedon Stamatopoulos (Director of Sourcing and Refining Argor-Heraeus)

The risks to source from ASM will be present regardless the existence of LBMA Standard v. 6, 8 or 10. If refiners do not engage with the ASM. The ASM material will take other routes and enter to international gold market. The more other routes take, the more value will be lost to LBMA members. So refiners have to engage and do it appropriately.

You choice matter!

Transforming lives through responsible artesanal and small-scale mining

But how? Buying from certified ASM

More than 370 companies from 33 countries work with Fairmined

1.6 tons and 6M USD of Fairmined Premium invested by miners

Ottimizzazione e riduzione del consumo d’acqua nei processi di trattamento superficiale

a speech by O. Balestrino

Introduzione

La presentazione si propone di evidenziare l’evoluzione dell’approccio ambientale nel corso degli anni da parte del legislatore e proporre alcune soluzioni tecniche per l’ottimizzazione e riduzione del consumo d’acqua nei processi di trattamento superficiale.

ECOTEAM spa progetta, realizza, manutiene impianti di trattamento acque ed acque reflue. Specializzata nel settore Trattamento e Finiture

Sviluppo della “Coscienza Ambientale” in Italia ed in Europa

Legge 319/1976 (Legge Merli)

D.lgs 152/2006

2019: “Industria 4.0”

2022: DNSH

La legge Merli indicava in maniera dettagliata le sostanze inquinanti, ponendo dei limiti al loro scarico nelle acque e alla loro concentrazione. Con riferimento agli scarichi, la ripartizione degli stessi ai fini della relativa disciplina e del conseguente trattamento sanzionatorio era fondata sulla loro provenienza; si disponeva inoltre che lo scarico effettuato in assenza della necessaria autorizzazione, concessa esclusivamente agli scarichi rispettosi dei limiti di accettabilità, fosse sempre soggetto a sanzione penale.

D.lgs 152 normativa di cui una sezione importante è dedicata appunto alla tutela delle acque dall’inquinamento e alla gestione delle risorse idriche.

Industria 4.0 / Ambiente

Impianti di trattamento acqua inseriti nel gruppo 2 allegato A dei materiali ammessi alla transizione 4.0, ovvero sistemi per l’assicurazione della qualità e della sostenibilità, con particolare riferimento alle due seguenti categorie:

componenti, sistemi e soluzioni intelligenti per la gestione, l’utilizzo efficiente e il monitoraggio dei consumi energetici e idrici e per la riduzione delle emissioni

filtri e sistemi di trattamento e recupero di acqua, aria, olio, sostanze chimiche, polveri con sistemi di segnalazione dell’efficienza filtrante e della presenza di anomalie o sostanze aliene al processo o pericolose, integrate con il sistema di fabbrica e in grado di avvisare gli operatori e/o di fermare le attività di macchine e impianti

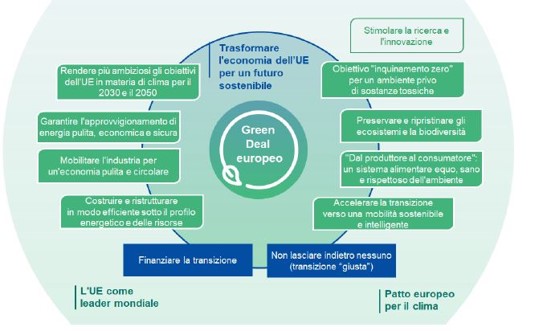

Green Deal Europeo

Il pilastro centrale di Next Generation EU è il dispositivo Recovery and Resilience Facility che, tra i vari obiettivi, si propone di sostenere interventi che contribuiscano ad attuare l’Accordo di Parigi e gli obiettivi di sviluppo sostenibile delle Nazioni Unite, in coerenza con il Green Deal europeo.

Obiettivo «Inquinamento zero» per un ambiente privo di sostanze tossiche

Do No Significant Harm

ll principio Do No SignificantHarm (DNSH) prevede che gli interventi previsti dai PNRR nazionali non arrechino nessun danno significativo all’ambiente: questo principio è fondamentale per accedere ai finanziamenti del RRF.

I piani devono includere interventi che concorrono per il 37% delle risorse alla transizione ecologica.

l principio DNSH si basa su quanto specificato nella “Tassonomia per la finanza sostenibile”, adottata per promuovere gli investimenti del settore privato in progetti verdi e sostenibili nonché contribuire a realizzare gli obiettivi del Green Deal.

Criteri del DNSH Il Regolamento individua sei criteri per determinare come ogni attività economica contribuisca in modo sostanziale alla tutela dell’ecosistema, senza arrecare danno a nessuno degli obiettivi ambientali

1 Mitigazione dei cambiamenti climatici

Un’attività economica non deve portare a significative emissioni di gas serra (GHG)

2 Adattamento ai cambiamenti climatici

Un’attività economica non deve determinare un maggiore

3 Uso sostenibile e protezione delle risorse idriche

Un’attività economica non deve essere dannosa per il buono stato dei corpi idrici (superficiali, sotterranei o marini) e determinare il deterioramento qualitativo o la riduzione del potenziale ecologico

4 Transizione verso l’economia circolare, con riferimento anche a riduzione e riciclo dei rifiuti

Un’attività economica non deve portare a significative inefficienze nell’utilizzo di materiali recuperati o riciclati, ad incrementi nell’uso diretto o indiretto di risorse naturali, all’incremento significativo di rifiuti, al loro incenerimento o smaltimento, causando danni ambientali significativi a lungo termine

5 Protezione e riduzione dell’inquinamento dell’aria, dell’acqua o del suolo

Un’attività economica non deve determinare un aumento delle emissioni di inquinanti nell’aria, nell’acqua o nel suolo

6 Protezione e ripristino della biodiversità e della salute degli eco-sistemi

Un’attività economica non deve dannosa per le buone condizioni e resilienza degli ecosistemi o per lo stato di conservazione degli habitat e delle specie, comprese quelle di interesse per l’Unione

Nace

Uno specifico allegato tecnico della Tassonomia riporta i parametri per valutare se le diverse attività economiche contribuiscano in modo sostanziale alla mitigazione e all’adattamento ai cambiamenti climatici o causino danni significativi ad uno degli altri obiettivi.

Basandosi sul sistema europeo di classificazione delle attività economiche (NACE), vengono quindi individuate le attività che possono contribuire alla mitigazione dei cambiamenti climatici, identificando i settori che risultano cruciali per un’effettiva riduzione dell’inquinamento. Il quadro definito dalla Tassonomia fornisce quindi una guida affidabile affinché le decisioni di investimento siano sostenibili ed è diventato un elemento cardine nei criteri di assegnazione delle risorse europee

C24 – Manufacture of basic metals

C24.4.1 – Precious metals production

C25 – Manufacture of fabricated metal products, except machinery and equipment

C25.6.1 – Treatment and coating of metals

ECOTEAM

«Inquinamento zero» per un ambiente privo di sostanze tossiche

Uso sostenibile e protezione delle risorse idriche

Un’attività economica non deve essere dannosa per il buono stato dei corpi idrici (superficiali, sotterranei o marini) e determinare il deterioramento qualitativo o la riduzione del potenziale ecologico

Protezione e riduzione dell’inquinamento dell’aria, dell’acqua o del suolo

Un’attività economica non deve determinare un aumento delle emissioni di inquinanti nell’aria, nell’acqua o nel suolo

DNSH nel T.F.

Progettazione impianti a basso impatto

Utilizzo di prodotti a bassa tossicità

Progettazione di impianti efficienti

Riuso e recupero delle soluzioni

Scarico liquido zero

Lavaggio

Riduzione dell’acqua

La progettazione del sistema di lavaggio è legata a:

1. Processo

a) Caratteristiche della soluzione di processo

b) Numero di lavaggi

c) Tipologia di lavaggi

2. Produzione

I. Superficie

II. Obiettivo finale

Importanza dei lavaggi: Riduzione dell’acqua

Un lavaggio in cascata permette una forte riduzione della portata d’acqua necessaria ed in prima approssimazione possiamo dire che la concentrazione nei lavaggi

DNSH e ZLD

Lo Scarico Liquido Zero può utilizzare diverse tecnologie e filosofie di progettazione ma il punto chiave è l’ultimo anello che è quasi sempre un sistema di evapo-concentrazione.

L’evapo-concentratore è un sistema che permette di concentrare delle soluzioni diluite eliminando/recuperando l’acqua.

Gli utilizzi principali sono:

1. Recupero di soluzioni diluite per essere riutilizzate come soluzioni di processo

2. Riduzione degli smaltimenti con recupero dell’acqua

EVAPO-CONCENTRATORI

Esistono diverse tecnologia di evapo-concentratori:

1.Pompa di calore

1. a serpentina immersa

2. a circolazione forzata

3. con raschiatore

2.Acqua calda

1. a singolo effetto

2. a doppio effetto

3. a triplo effetto

3.Ricompressione Meccanica dei Vapori

1. a circolazione naturale

2. a circolazione forzata

3. falling film

1. Con compressore a lobi

2. Con compressore centrifugo

CONCLUSIONI

La riduzione del consumo d’acqua, fino al punto estremo dello Scarico Liquido Zero, nei processi di trattamento superficiale persegue “l’obiettivo Inquinamento zero per un ambiente privo di sostanze tossiche”.

I costi di esercizio con le opportune tecniche possono essere molto vantaggiosi.

Optimization and reduction of water consumption in surface treatment processes

a speech by O. Balestrino

Preface

The presentation aims to highlight the evolution of the environmental approach over the years by the legislator and propose some technical solutions for the optimization and reduction of water consumption in surface treatment processes.

ECOTEAM spa designs, builds, maintains water and wastewater treatment plants.Specialized in the Treatment and Finishing sector

Development of “Environmental Consciousness” in Italy and Europe

Legge 319/1976 (Legge Merli)

D.lgs 152/2006

2019: “Industria 4.0”

2022: DNSH

The Merli law indicated in detail the polluting substances, placing limits on their discharge into water and their concentration. With reference to discharges, the distribution of the same for the purposes of the relative regulations and the consequent sanctioning treatment was based on their origin; it was also established that unloading carried out in the absence of the necessary authorization, granted exclusively to unloading in compliance with the limits of acceptability, was always subject to a criminal sanction.

Legislative Decree 152 of which an important section is dedicated precisely to the protection of water from pollution and the management of water resources.

Industry 4.0 / Environment

Water treatment plants included in group 2 Annex A of the materials admitted to transition 4.0, or systems for quality and sustainability assurance, with particular reference to the following two categories :

components, systems and intelligent solutions for the management, efficient use and monitoring of energy and water consumption and for the reduction of emissions

filters and treatment and recovery systems for water, air, oil, chemicals, dust with signaling systems of filtering efficiency and the presence of anomalies or substances alien to the process or dangerous, integrated with the factory system and able to warn operators and / or to stop the activities of machines and plants

European Green Deal

The central pillar of Next Generation EU is the Recovery and Resilience Facility which, among other objectives, aims to support interventions that contribute to implementing the Paris Agreement and the United Nations Sustainable Development Goals, in line with the European Green Deal.

Objective “Zero pollution” for an environment free of toxic substances

Do No Significant Harm

The Do No Significant Harm principle (DNSH) states that the actions outlined in national NRRPs may not cause any significant harm to the environment: this is a fundamental principle for accessing funding from the RRF.

In addition, the plans must include actions which contribute 37% of the resources to the ecological transition.

The DNSH principle is based on the provisions of the “Taxonomy for Sustainable Finance” adopted to promote private sector investment in green and sustainable projects and help achieve the goals of the Green Deal.

Criteria of DNSH The Regulation identifies six criteria for determining how each economic activity substantially contributes to protecting the ecosystem, without undermining any of the environmental goals

1 Climate change mitigation

An economic activity must not lead to significant emissions of greenhouse gases (GHG)

2 Climate change adaptation

An economic activity must not have an increased negative impact on the current and future climate, on the activity itself or on people, nature or property

3 Sistainable use and protection of water and marine resources

An economic activity must not be detrimental to the good health of water bodies (surface, groundwater or marine) or harm its quality or reduce its ecological potential

4 Transition to the circular economy, including waste prevention and recycling

An economic activity must not result in significant inefficiencies in the use of recovered or recycled materials, increase the direct or indirect use of natural resources, or significantly increase waste or the burning or disposal thereof, causing significant long-term environmental damage

5 Prevention and reduction of air, water and soil pollution

An economic activity must not cause increased emissions of pollutants in the air, water or soil

6 Protection and restoration of biodiversity and health of ecosystems

An economic activity must not harm the good condition and resilience of ecosystems or the conservation status of habitats and species, including those of interest to the Union.

Nace

A specific technical annex of the Taxonomy sets out the parameters for evaluating whether different economic activities substantially help with climate change mitigation and adaptation or whether they cause significant harm to one of the other goals. Based on the Statistical Classification of Economic Activities in the European Community (NACE), the activities that can help to mitigate climate change are then determined, identifying the sectors that are crucial for an effective reduction in pollution. The framework defined in the Taxonomy therefore provides a reliable guide for making sustainable investment decisions, and has become a core component of the criteria for allocating European resources

C24 – Manufacture of basic metals

C24.4.1 – Precious metals production

C25 – Manufacture of fabricated metal products, except machinery and equipment

C25.6.1 – Treatment and coating of metals

ECOTEAM

«Zero pollution» for an environment free of toxic substances

Sistainable use and protection of water and marine resources

An An economic activity must not be detrimental to the good health of water bodies (surface, groundwater or marine) or harm its quality or reduce its ecological potential

Prevention and reduction of air, water and soil pollution

An economic activity must not cause increased emissions of pollutants in the air, water or soil

DNSH in F.T.

Low impact plant design

Use of low toxicity products

Design of efficient systems

Reuse and recovery of solutions

Zero liquid discharge

RINSING

Water reduction

The design of the washing system is linked to:

1. Process

a) Characteristicsof the process solution

b) Numbers of rinsing

c) Type of rinsing

2. Production

I. Surface

II. Final goal

Importance of rinsing: Water reduction

A cascade rinsing allows a strong reduction of the necessary water flow and as a first approximation we can say that the concentration in the washes Xn

DNSH e ZLD

The Zero Liquid Discharge can use different technologies and design philosophies but the key point is the last link which is almost always an evaporation-concentration system.

The evaporator-concentrator is a system that allows you to concentrate diluted solutions by eliminating / recovering water.

The main uses are :

1. Recovery of diluted solutions to be reused as process solutions

2. Reduction of disposal with water recovery

EVAPO-CONCENTRATORS

There are different technologies of evapo-concentrators:

Heat pump

with immersed coil

forced circulation

with scraper

Hot water

single effect

double effect

triple effect

Mechanical Vapour Recompression

1. Natural circulation

2. forced circulation

3. falling film

a) With lobe compresso

CONCLUSIONI

The reduction of water consumption, up to the extreme point of Zero Liquid Discharge, in the surface treatment processes pursues “the goal of zero pollution for an environment free of toxic substances“

Operating costs with the appropriate techniques can be very advantageous.

Author: World Commission on Environment and Development

Year: 1987

For the first time, the report identifies Sustainability as:

The condition of a development capable of “ensuring the satisfaction of the needs of the present generation without compromising the possibility of future generations to realize their own”

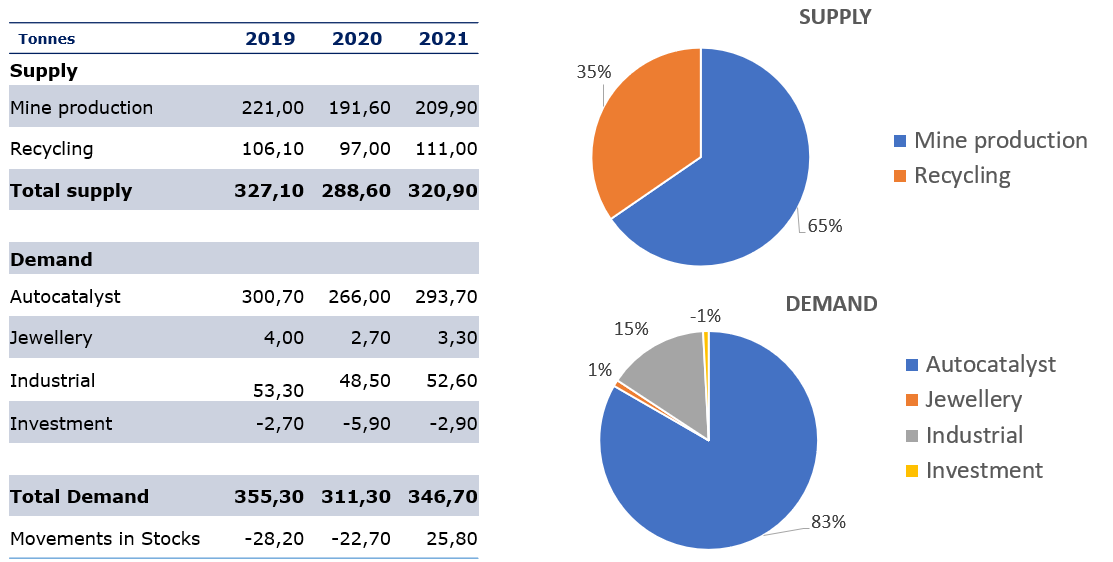

Precious Metals

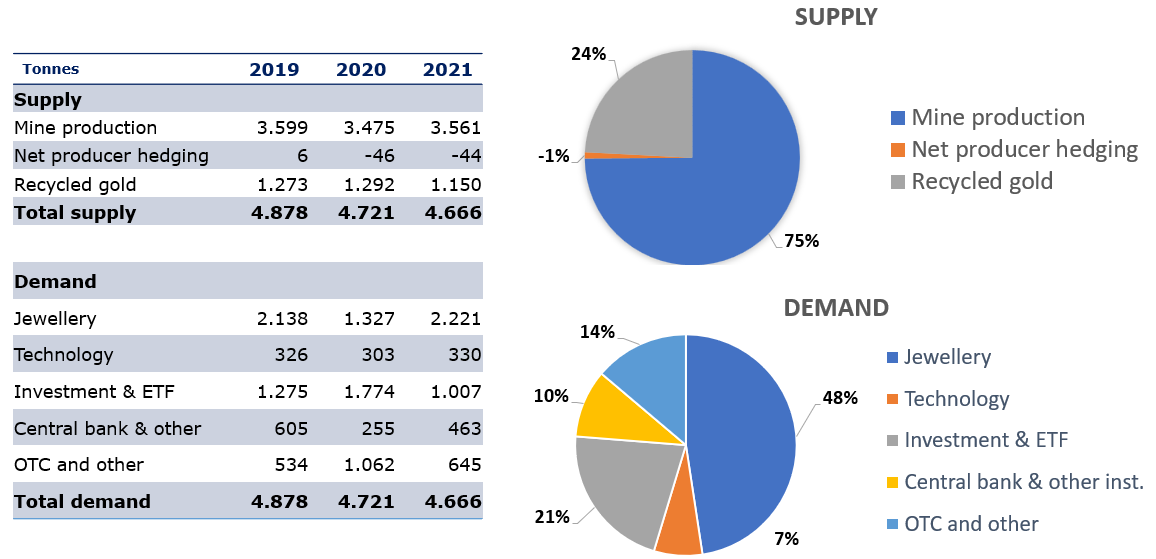

Supply and Demand: Gold

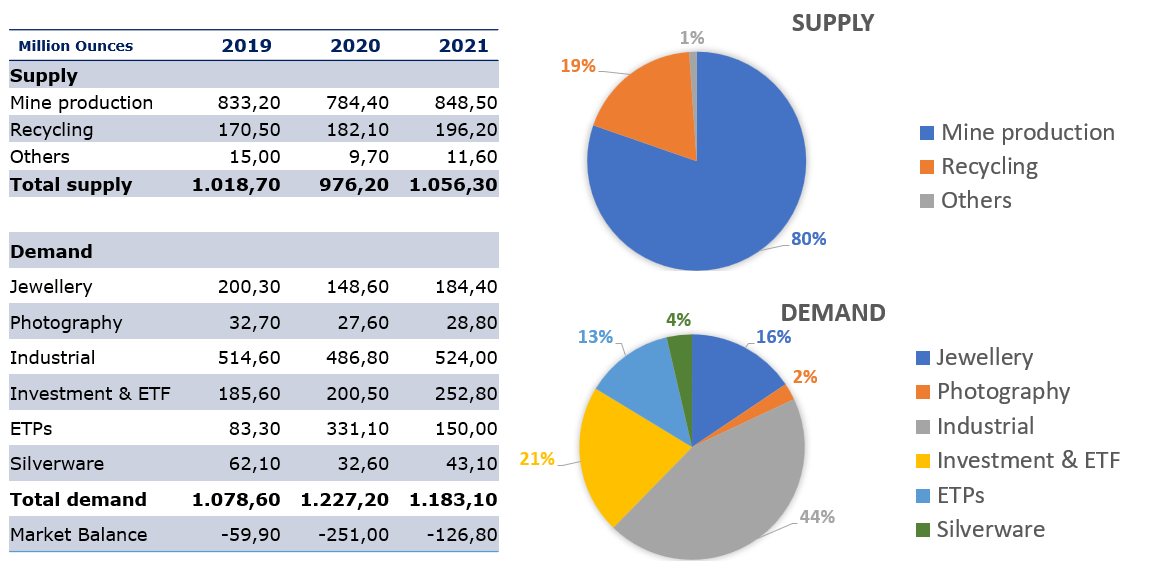

Supply and Demand: Silver

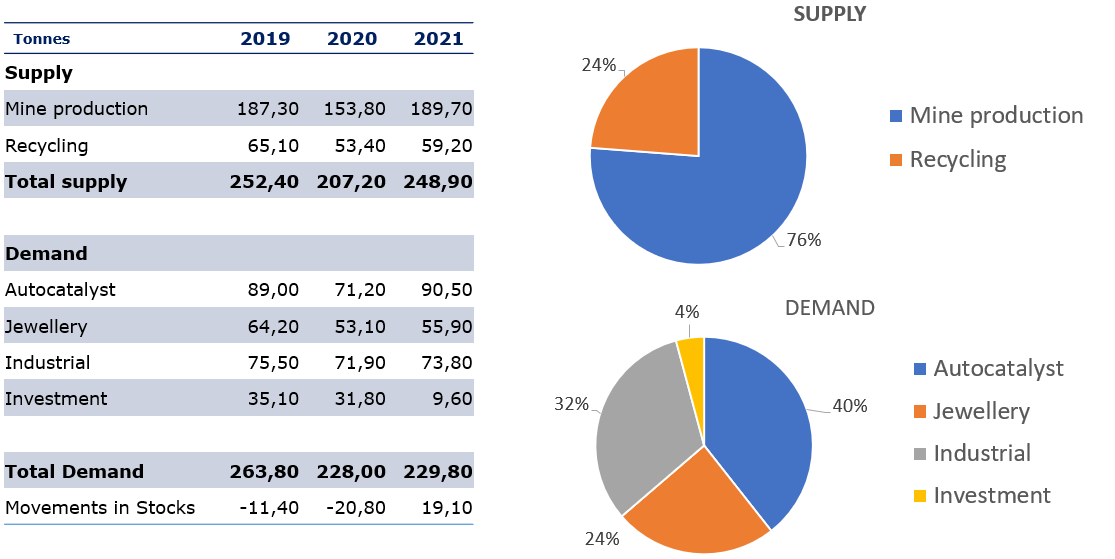

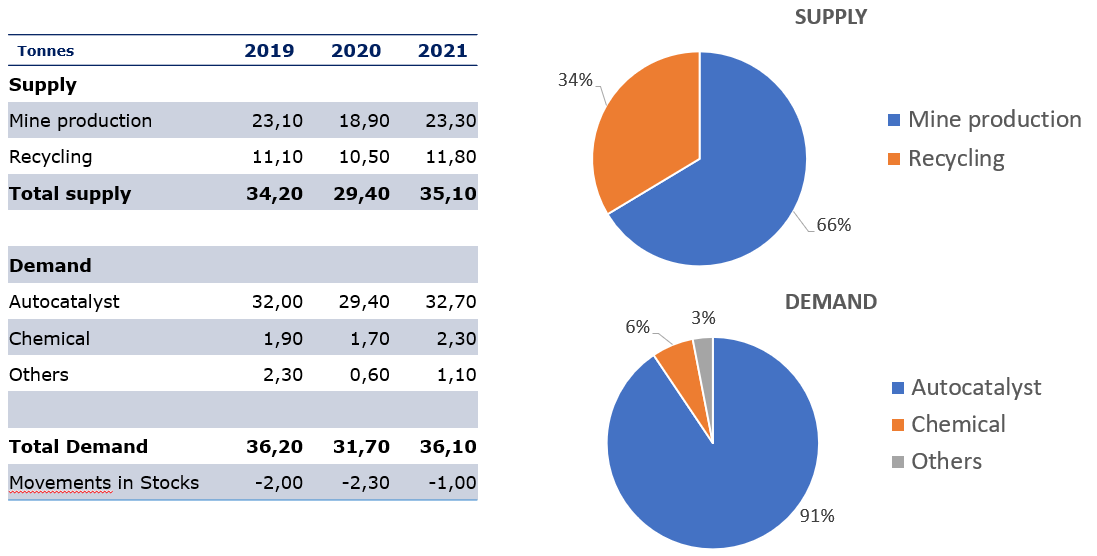

Supply and Demand: Platinum

Supply and Demand: Palladium

Supply and Demand: Rhodium

Supply Sources:

Mining

Refining

Grandfathered

Kinf of Mines

Open Pit Mine

Underground Mine

Artisanal Mine

Recycled Sources from Refining

Industrial Scraps

Jewelry Scraps

Disinvestments

Central Bank Sales

Electronic Scraps

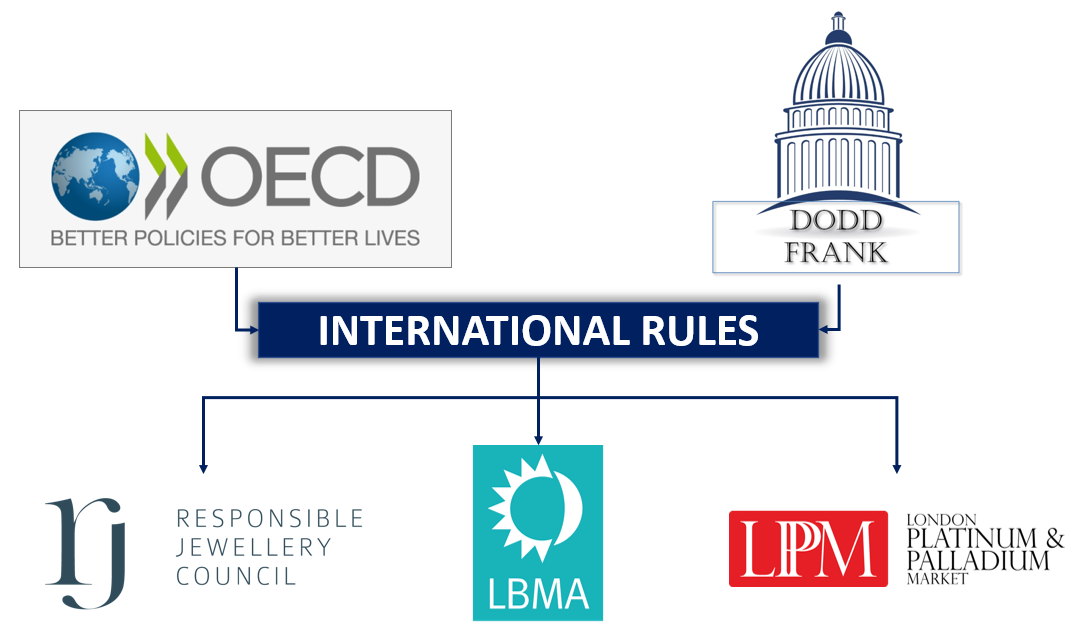

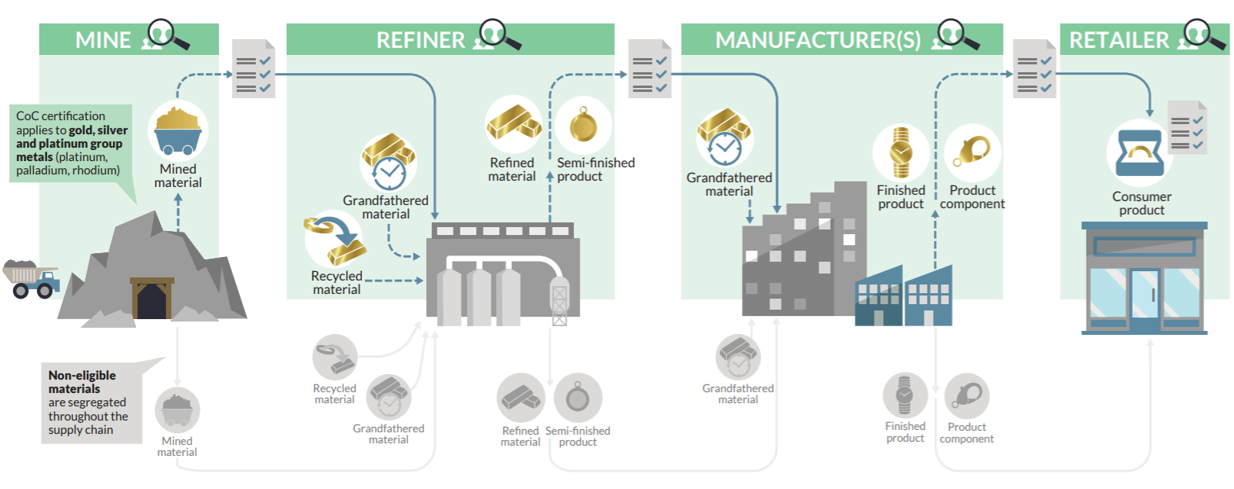

Rules and Associations

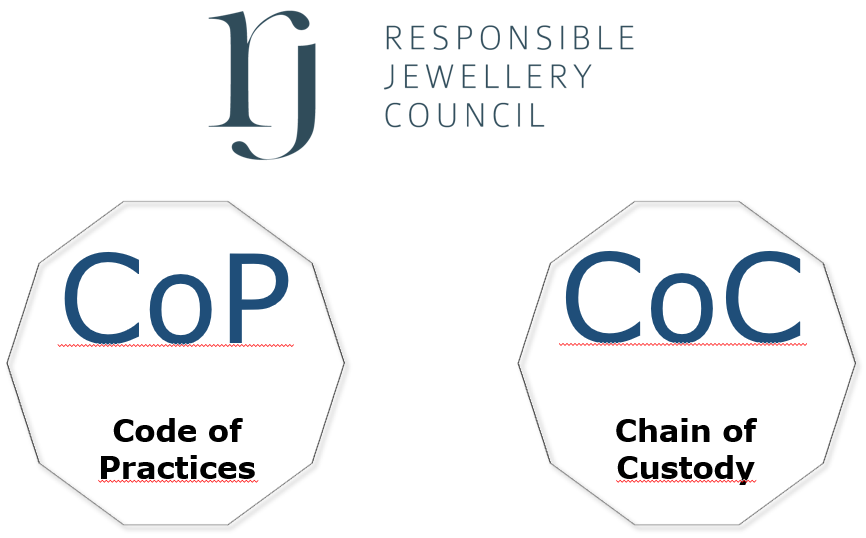

Responsible Jewellery Council

Individual provisions of the COP

Overview of the RJC CoC Standard

Sustainability on Precious Metals

PROVENANCE CLAIM

A documented claim made through the use of descriptions or symbols, relating to Precious Metals and specifically relate to their:

Origin – Geographical origin of materials, for example country, region, mine or corporate ownership of the Mining Facility/ies;

Source – Type of source, for example recycled, mined, artisanally mined, or date of production;

Practices – Specific practices applied in the supply chain relevant to the Code of Practices, including but not limited to, standards applicable to extraction, processing or manufacturing, conflict-free status, or due diligence towards sources.

Claims supported by evidence to avoid:

Greenwashing

Misleads consumers

Unfair to competitors who make legitimate efforts

All precious metals used by Legor Group S.p.A. are 100% RJC CoC compliant and 100% from recycled sources (Au, Ag, Pt, Pd, Rh)

Diamante sintetico: un problema commerciale per il futuro?

una relazione di Antonello Donini

Stiamo parlando di DIAMANTE SINTETICO. Carbonio (C) cristallizzato nel sistema cubico disposto nel reticolo secondo la configurazione spaziale tetraedrica. Come accade nel diamante naturale tale configurazione conferisce a questo materiale proprietà che lo rendono unico nel suo genere.

Non parliamo quindi di una imitazione ma di vero e proprio diamante prodotto con metodi artificiali di sintesi fatti dall’uomo e non dalla natura.

I primi tentativi di realizzare in laboratorio l’esatta controparte sintetica del diamante sono databili intorno alla fine del 19° secolo, ma il primo successo storicamente documentato risale alla prima metà degli anni ’50 del 20° secolo, quando i ricercatori dell’americana General Electric hanno sintetizzato i primi piccoli cristalli di diamante.

Sempre la General Electric, circa 20 anni dopo, ha realizzato i primi diamanti sintetici aventi dimensioni sufficienti per poter avere un utilizzo come gemma, seguita negli anni ’80 dalla giapponese Sumitomo, dalla De Beers e verso l’inizio degli anni ’90, da laboratori russi.

Metodi di sintesi

Metodo di produzione HPHT

Il metodo si basa sulle condizioni che hanno permesso in natura la formazione del diamante ovvero alte pressioni ed alte temperature.

All’interno delle celle di reazione contenenti cristalli-seme, una lega/soluzione metallica (ad esempio nickel e ferro) che funge da fondente/catalizzatore, il nutriente (solitamente grafite) viene esposto a condizioni di alte pressioni ed alte temperature (tra 1400 e 1600°C e tra 50 e 60 kbar) grazie a elementi riscaldanti e presse. Il carbonio si dissolve nel fondente e si deposita quindi sui cristalli seme posti solitamente in una zona della cella con temperatura inferiore sotto forma di diamante.

Metodo HPHT BARS

Metodo HPHT TOROID

Metodo HPHT CUBOID

Una importante problematica da affrontare per questo metodo di sintesi è quello di tenere lontana la presenza di azoto responsabile di una colorazione verde giallo alla bruna dei cristalli sintetizzati. L’utilizzo di nuove leghe metalliche utilizzate come fondenti, con l’aggiunta di particolari elementi (come alluminio, cobalto o rame) che permettono di fissare l’azoto facendo in modo che non rientri nel reticolo del diamante.

Si ottengono così diamanti incolori (tipo Iia) o con lieve colorazione bluastra per la presenza di lievissime quantità di boro (tipo IIb).

DIAMANTE SINTETICO CVD

Ha il grosso vantaggio di avvenire a basse pressioni, nell’ordine di 10-200 torr.

Nella camera viene creato un plasma che rompe la molecola di metano o altro gas contenente C.

Il carbonio si va quindi poi a depositare sotto forma di diamante su un substrato solitamente costituito da sottili semi di diamante.

Elementi utili alla identificazione

I diamanti sintetici incolori CVD sono in generale del tipo IIa ovvero composti da solo carbonio.

Per eliminare una possibile componente bruna presente nei diamanti cristallizzati con questo metodo dovuta a dislocazioni, vengono sottoposti a un post trattamento HPHT in grado di eliminarla.

Al microscopio i diamanti sintetici HPHT mostrano spesso caratteristiche figure di crescita, correlate ai settori di crescita cubici e ottaedrici.

È possibile rilevarle in corrispondenza di zonature di diversa fluorescenza o nella distribuzione del colore all’interno della pietra che segue questi settori di crescita. Le inclusioni caratteristiche, ma non sempre presenti, sono residui di fondente che si presentano come inclusioni nere e opache con lustro metallico.

Zonature di colore e linee di struttura in diamante sintetico HPHT che seguono i settori di crescita

Le inclusioni caratteristiche, ma non sempre presenti, sono residui di fondente che si presentano come inclusioni nere e opache con lustro metallico o estesi gruppi di inclusioni puntiformi (probabilmente minute particelle di fondente disperso).

Inclusioni di fondente metallico in diamanti sintetici incolori HPHT

Esempi di inclusioni in diamante sintetico HPHT

I diamanti sintetici CVD potrebbero avere minute inclusioni scure (residui carboniosi) con aloni di tensione probabilmente generati da un post trattamento termico utilizzato per migliorare il colore delle gemme.

Esempi di inclusioni in diamanti cvd

Molti diamanti sintetici HPHT mostrano una caratteristica fluorescenza da gialla a verde giallastra agli UVL (365 nm) e agli UVC (254 nm).

Le impurità che vengono assorbite nella struttura del diamante sintetico durante la sua crescita tendono a concentrarsi ciascuna in determinati settori di crescita, ciò origina caratteristiche figure di fluorescenza, a forma di croce o ottagonali, mai viste in diamanti naturali.

Spesso, a differenza di quanto accade nei naturali, la reazione è più intensa all’onda corta che a quella lunga.

I diamanti naturali generalmente mostrano una fluorescenza più o meno marcata di colore blu (più raramente gialla e, meno comunemente ancora, verde o rosa), abbastanza uniforme e, comunque, più marcata all’onda lunga che all’onda corta.

Effetti di luminescenza che seguono le direzioni di crescita cubo-ottaedriche in un diamante

La presenza di fosforescenza solitamente persistente (rarissima in natura e atipica nelle pietre incolori) è un buon segno identificativo. Sono infatti i diamanti di tipo IIb estremamente rari in natura (contenenti boro) che presentano questo effetto solitamente di breve durata.

Una caratteristica particolare dei diamanti prodotti con il metodo HPHT è quello di mostrare poche o lievi birifrangenze anomale al contrario dei diamanti naturali. Nei sintetici CVD le birifrangenze anomale sono generalmente simili a quelle dei diamanti di tipo IIa naturali ovvero con una specie di graticcio, spesso orientato secondo la direzione di deposizione dei cristalli.

Esistono però cristalli sintetici CVD di qualità “ottica” (QUINDI OTTICAMENTE PERFETTI ED OMOGENEI) privi di birifrangenze anomale.

Birifrangenze anomale in diamante sintetico HPHT. Quando presenti assumono la forma di una croce

Birifrangenze anomale in diamante sintetico CVD

Identificazione certa solo attraverso tecniche analitiche avanzate

La spettrofotometria IR (infrarosso) è un ottimo aiuto per riconoscere la tipologia del diamante ovvero per verificare la presenza o assenza di tracce di alcuni elementi fondamentali. SI hanno così potenziali informazioni per isolare tipologie di diamante che potrebbero essere compatibili con una produzione sintetica.

I Diamanti sintetici incolori sono di tipo IIa (azoto presente in quantità talmente piccola da non poter essere rilevato strumentalmente con IR), mentre quelli blu, come i loro analoghi naturali, sono di tipo IIb (presenza di boro). La presenza del tipo IIb ovvero di tracce di boro è riscontrabile spesso in moltissimi diamanti sintetici incolori. Sono stati anche visti in commercio diamanti sintetici di colore rosa dovuto ad un post trattamento per irraggiamento e successivo riscaldamento a bassa temperatura. E’ bene ricordare che le prime produzioni, proprio per la presenza di azoto prevedevano colorazioni nel giallo con diverse sfumature di bruno o bruno verdastro. Alcuni diamanti di questo tipo trattati per irraggiamento hanno assunto un vivacissimo colore rosso.

Allo spettrofotomentro UV-VIS-NIR la componente Ib presente nei diamanti sintetici giallo verdi genera un assorbimento a partire dai 500 nm verso l’ultravioletto. Molti diamanti mostrano, una serie di assorbimenti tra 470 nm e 700 nm, dei quali il più evidente è a 658 nm. Questi picchi sono dovuti alla presenza di nickel all’interno della struttura cristallina presente nel catalizzatore. I diamanti incolori sintetici di tipo IIa sono trasparenti sino a 270 nm.

Presenza di elementi come nickel, ferro, alluminio, cobalto, rame o gli altri metalli impiegati nella crescita, possono essere identificati mediante un’analisi chimica con fluorescenza ai raggi X (EDXRF).

Attraverso la Fotoluminescenza è possibile rilevare centri di colore diagnostici grazie alle tracce di impurità presenti quindi riconoscere la natura sintetica.

La osservazione degli effetti di luminescenza ad uv molto corti può essere molto utile per riconoscere i diamanti sintetici.

Quadro della situazione commerciale

I produttori di diamanti sintetico sostengono che:

I diamanti prodotti artificialmente in laboratorio hanno essenzialmente la stessa composizione chimica, struttura cristallina, proprietà ottiche e fisiche dei diamanti estratti dalle miniere: sono quindi diamanti al 100%. L’unica differenza tra i diamanti sintetici e quelli estratti è che uno è stato creato all’interno ed estratto dalla Terra e l’altro è stato creato in un laboratorio all’avanguardia.

Sono numerosi i produttori che sintetizzano diamante soprattutto per scopi industriali.

In gioielleria la dimensione delle gemme sfaccettate ha raggiunto dimensioni decisamente importanti: sono state viste gemme di oltre 10 ct. Ma la maggiore diffusione di questo prodotto si ha su gemme fino ad un max di 2,00 ct e nei lotti melèe (da meno di un punto fino a 0,25 ct).

Costante crescita e diffusione nel settore orafo dell’utilizzo di questo materiale gemmologico, trascinato dall’intensivo e sempre maggiore impiego industriale di questo materiale. Ampiamente utilizzato negli strumenti come superabrasivi, mole, utensili da taglio, strumenti di perforazione e lucidatura, prodotti dell’industria automobilistica, medica, aerospaziale ed elettronica.

Per i costi di manifattura e per importanza di mercato fanno la parte del leone i paesi asiatici, seguiti dal nord America.

Commercialmente stanno avendo un forte spunto e diffusione soprattutto negli USA e in Giappone.

A fornire un forte discapito per chi tratta il naturale, la FTC statunitense (Federal Trade Commission, organo legislativo commerciale) ha permesso che queste sintesi potessero essere chiamate come “grown diamonds”. Ha inoltre stabilito che il “diamante sintetico” è da considerarsi come vero e proprio “diamante” permettendo ai produttori di sintetici di commercializzare i loro prodotti come «reali» / «veri» (real diamonds).

Il resto del mondo e le norme ISO internazionali prevedono che questo materiale gemmologico debba essere chiamato, ai fini della chiarezza nei confronti del consumatore solo come “diamante sintetico” al pari di qualsiasi altra sintesi. Nessuna altra definizione o semplificazione è ammessa. ISO 18323:2015

Il costo di questo materiale è attualmente inferiore al naturale di circa il 30-40% ma sono previste ulteriori diminuzioni dovute ad una sempre maggiore diffusione e alla riduzione dei costi di produzione.

I diamanti sintetici rappresentano attualmente circa Il 2% del mercato globale. Ci si aspetta che entro il 2030 tale quota possa salire al 10%. Per pietre con peso attorno al 0,50-1,50 ct, adatte ad un impiego come solitario ovvero per un anello da fidanzamento la quota del 7,5% potrebbero essere raggiunta già nel 2020.

Per il «melèe» si potrebbe arrivare ad una quota del 15% nei prossimi due anni.

La diffusione di questo materiale nel melèe potrebbe essere intensificata da una progressiva scarsità di diamanti estratti in natura in quanto è attesa la chiusura della miniera di Argyle (ormai quasi esausta) che attualmente fornisce la maggior parte dei diamanti piccoli del mondo.

Difficile quindi fare oggi delle previsioni su quale sarà il reale impatto di questo materiale sul mercato dei preziosi.

Le nuove generazioni sembrano, dagli studi di marketing, positivamente favorevoli all’utilizzo di questo nuovo materiale in ornamentazione.

Il diamante sta perdendo quel fascino di pietra simbolo di rarità e amore eterno per raggiungere sempre più lo status di gemma a larga diffusione. I consumatori iniziano a percepire i diamanti sintetici come allettanti: è possibile avere gemme più grandi a prezzi più bassi e, soprattutto, fare un investimento «privo di sensi di colpa». È attiva una importante operazione mediatica per pubblicizzare queste gemme come maggiormente “etiche” rispetto le naturali. I giovani, essendo giustamente orientati all’ambiente e al non sfruttamento di risorse naturali e soprattutto umane, mostrano maggiore interesse per questo tipo di gemme, rispetto le generazioni precedenti coinvolte maggiormente sulla unicità e rarità del singolo gioiello.

Grossi nomi dello spettacolo e del mondo web come Di Caprio, Lady Gaga, Penelope Cruz o i possessori di Facebook, Twitter e eBay hanno pubblicizzato o persino finanziato strutture per la produzione di diamanti sintetici, credendo nel loro futuro. La Diamond Foundry uno degli ultimi produttori statunitensi comparsi sul mercato ha dichiarato di essere attualmente l’unico produttore di diamanti certificato “carbon neutral”, in quanto i suoi diamanti sono fabbricati in un reattore al plasma ad energia idroelettrica. Sostiene inoltre che: “l’estrazione mineraria ha un impatto ambientale maggiore rispetto a qualsiasi altra attività umana. Per un singolo carato di diamante, devono essere scavate circa 250 tonnellate di terra, e vengono rilasciati notevoli quantità di inquinamento atmosferico con l’emissione pesante di anidride carbonica”.

De Beers attraverso il marchio LIGHTBOX ha iniziato la commercializzazione on-line di linee di gioielleria con diamanti sintetici incolori, azzurri e rosa ad un costo molto basso cercando di accaparrarsi una importante fetta di mercato mondiale. (1.00 ct 800,00 US$ – 0.50 ct 400.00 US$ – 0.25 ct 250.00 US$).

Dagli studi più del 60% degli intervistati sarebbero disposti, interessati all’acquisto di un diamante sintetico su un anello di fidanzamento, per il costo inferiore del materiale permettendo così di avere gemme di dimensione maggiore ad un costo inferiore.

I consumatori con disponibilità economica solitamente più legati al fascino, al mistico all’unico e all’irripetibile…sembrano invece mostrare molto interesse per questo materiale.

I produttori di diamanti sintetici sono stati in grado di interessare i cosiddetti «millennials» promuovendo il Lab Grown Diamond come high-tech, innovativo e pulito.

In tutti gli aspetti della loro vita cercano marchi, aziende e prodotti che ritengono trasparenti, socialmente e rispettosi dell’ambiente.

Il consumatore non crede ormai più nel valore dei diamanti o del gioiello in generale.

Ci sono infatti stati nel tempo diversi fattori che hanno diffuso sfiducia nel settore.

Operatori commerciali poco trasparenti

Scarsa conoscenza dei materiali e del mercato da parte degli operatori

Scarsa resa dei diamanti da investimento

Poche certezze

Occorre però tener conto che: un diamante naturale anche se di brutta qualità avrà sempre un possibile acquirente. Non esiste invece un mercato secondario per i diamanti sintetici, soprattutto perché i commercianti di diamanti attuali tendenzialmente non li trattano. Il «buon affare», il risparmio che si può avere acquistando un diamante sintetico, sfuma quando si pensa al fatto che sarà impossibile rivenderlo.

Al momento il quadro è decisamente confuso, poco chiaro. Gli operatori del mondo, dati gli interessi economici che ruotano attorno al materiale naturale, sono decisamente preoccupati e spaventati dalla improvvisa diffusione e dal numero delle operazioni mediatiche che stanno ruotando attorno al diamante sintetico.

Ma se guardiamo al passato quello che sta accadendo ora è stato promosso nello stesso ed identico modo in passato quando DeBeers all’inizio del secolo scorso attraverso operazioni mediatiche mirate e personaggi dello spettacolo (pensiamo a Marylin Monroe e alla frasi «i diamanti sono i migliori amici delle ragazze» e «li diamante è per sempre») ha diffuso l’uso del diamante in gioielleria in modo che potesse diventare per tutti «simbolo di vero amore eterno».

Quindi difficile dare una risposta al quesito iniziale anzi, possiamo aggiungere ora un altro quesito: “il diamante sintetico potrebbe essere una opportunità?”

Lab-grown diamond: is it a commercial problem for the future?

a speech by Antonello Donini

We are talking about

SYNTHETIC DIAMOND

Crystalized carbon (C) in the cubic system and arranged tetrahedrally within the grid.

As with natural diamond, this configuration gives the material properties that make it unique.

Therefore, we are not speaking of an imitation but of an authentic diamond produced by artificial synthesis methods made by man rather than by nature.

Initial attempts to produce the exact synthetic counterpart of diamond in the laboratory date back to the late 19th century, although the first historical success was recorded in the early 1950s when researchers at the American company, General Electric, synthetized the first small diamond crystals.

About 20 years later, General Electric was also the first to create synthetic diamonds large enough to be used as gems. This success was followed by the Japanese company, Sumitomo, and De Beers in the 1980s and by Russian laboratories in the ‘90s.

Synthesis methods

The HPHT production method

This method is based on the conditions that led to diamond formation in nature, i.e. high pressure and high temperature.

Crystal seeds, a metal alloy/solution (e.g. nickel and iron), which acts as an amalgamate/catalyst, and the nutrient (usually graphite) are placed inside the reaction cell and exposed to high pressure and high temperatures (between 1400 and 1600° C and between 50 and 60 kbars) using heating elements and presses. The carbon dissolves into the amalgamate and then deposits on the crystal seeds in diamond form, usually in a part of the cell where the temperature is lower.

HPHT method BARS

HPHT method TOROID

HPHT method CUBOID

An important problem to face in this synthesis method is keeping any nitrogen responsible for the yellow-green to brown colouring of the synthetized crystals at bay. Using new metal alloys as amalgamates, with the addition of particular elements (such as aluminium, cobalt or copper) fixes the nitrogen so that it cannot go back into the diamond grid. Colourless diamonds (like lla diamonds) or those with a slightly bluish colour due to a very slight quantity of boron (type Ilb), are thus obtained.

CVD SYNTHETIC DIAMONDS

This method has the advantage of taking place at low pressures of about 10-200 torr. A plasma is created in the chamber that breaks the molecule of the methane or other carbon-containing gas. The carbon is then deposited in diamond form on a substrate usually made of tiny diamond seeds.

Useful identification elements

Colourless, CVD synthetic diamonds are generally of the Ila type, i.e. purely carbon.

In order to eliminate any possible brown components in crystalized diamonds that may occur with this method due to dislocations, the stones are subsequently subjected to an HPHT treatment which can eliminate them.

Under the microscope, synthetic HPHT diamonds often show characteristic growth shapes, correlated to sectors of cubic and octahedral growth.

This growth can be found in zonings of various fluorescence or in the colour distribution within the stone that follows these growth sectors. Characteristic inclusions, not always present, are amalgamate residues that look like black and opaque inclusions with a metallic shine.

Colour zoning and structure lines in HPHT synthetic diamonds that follow the growth sectors

Characteristic inclusions, not always present, are amalgamate residues that look like black and opaque inclusions with a metallic shine or large groups of punctiform inclusions (probably minute particles of dispersed amalgamate).

Metal amalgamate inclusions in colourless HPHT synthetic diamonds

Examples of inclusions in HPHT synthetic diamonds

CVD synthetic diamonds can have minute, dark inclusions (carbon residues) with tension streaks probably generated by subsequent heat treatment used to improve the colour of the gems.

Examples of inclusions in CVD diamonds

Many HPHT synthetic diamonds have a typical fluorescence that ranges from yellow to a yellowish green under UVL (365 nm) and UVC (254 nm).

The impurities that are absorbed in the synthetic diamond structure during its growth tend to concentrate in particular growth sectors, that is, they generate characteristic cross-shaped or octagonal fluorescence shape, that are not found in natural diamonds.

Unlike natural diamonds, the reaction is more intense at short wave than long wave.

Natural diamonds generally show a variable degree of quite uniform blue fluorescence (yellow is much rarer and green or pink even more so) which is, in any case, more noticeable at long wave than at short wave.

Luminescence effects that follow cubo-octahedral growth directions in a diamond

The usually persistent presence of phosphorescence (extremely rare in nature and atypical in colourless stones) is a good identification sign. In fact, llb-type diamonds are extremely rare in nature (containing boron) which only usually have this effect for a short time.

A particular characteristic of diamonds produced with the HPHT method is that they have few or only slight abnormal birefringencies, unlike natural diamonds. In CVD synthetic diamonds, abnormal birefringencies are generally similar to those in natural, lla-type diamonds, that is, they have a kind of trellis, often going in the same direction as the crystal deposit.

There are, however, CVD synthetic crystals with an «optic» quality (THEREFORE OPTICALLY PERFECT AND HOMOGENOUS) with no abnormal birefringencies.

Abnormal birefringencies in HPHT synthetic diamond. When present, they are cross-shaped

Abnormal birefringencies in CVD synthetic diamond

Definite identification is only possible with advanced analytical techniques

Infra-red spectrophotometry is ideal for helping to recognize the type of diamond, or rather, to check for the presence or absence of traces of some fundamental elements. IRS thus has the potential information for isolating diamond types that could be compatible with synthetic production.

Colourless synthetic diamonds are type lla (nitrogen in such small quantities that it cannot be detected instrumentally with IR), while blue diamonds, like their natural counterparts, are type llb (presence of boron). Type llb, or rather, traces of boron, can often be found in many colourless synthetic diamonds. Pink synthetic diamonds have also been seen on the market due to a subsequent irradiation treatment and heating at low temperatures. It should be remembered that, due to the presence of nitrogen, the initial productions foresaw yellow colouring in various shades of brown or greenish-brown. Some diamonds of this type, treated with irradiation, have been known to become a very bright red.

In UV-VIS-NIR spectrophotometry, the lb component in yellow-green synthetic diamonds generates an absorption that starts at 500 nm and goes towards ultraviolet. Many diamonds show a series of absorptions, between 470 nm and 700 nm, with a more evident absorption at 658 nm. These peaks are due to the presence of nickel within the crystalline structure in the catalyst. lla-type colourless synthetic diamonds are transparent up to 270 nm.

The presence of elements like nickel, iron, aluminium, cobalt, copper or other metals used in the growth, can be identified through chemical analysis with X-ray fluorescence (EDXRF).

Centres of diagnostic colour can be detected through photoluminescence due to traces of impurities. In this way the synthetic nature can be recognized.

Observing the effects of luminescence under extremely short uv can be very useful in recognizing synthetic diamonds.

Overview of the market situation

Synthetic diamond producers claim that:

Lab-grown diamonds essentially have the same chemical composition, crystalline structure, optical and physical properties as diamonds extracted from mines: they are, therefore, 100% diamonds. The only difference between synthetic and mined diamonds is that one was created within the Earth and extracted while the other was created in a cutting-edge laboratory.

Numerous producers synthetize diamond above all for industrial purposes.

In jewellery, the size of multi-faceted gems has reached decidedly significant dimensions: gems of over 10 ct have been seen. But the greatest distribution of this product is with gems up to a maximum of 2.00 ct and in melee lots (from less than a dot to up to 0.25 ct).

Constant growth and distribution of this gemmological material in the jewellery sector is towed by its intensive and ever-greater use in industry. It is widely used in instruments such as super sanders, grinding wheels, cutting tools, tools for drilling and polishing, products used in the automobile, medical, aerospace and electronic industries.

Due to their manufacturing costs and market importance, synthetic diamonds play a leading role in Asian countries, followed by North America.

Commercially-speaking, they are receiving considerable success and distribution in the USA and Japan.

As a detrimental measure against those dealing in the natural stone, the American FTC (Federal Trade Commission, the legislative trade authority) has allowed these synthetic stones to be called “grown diamonds”. It has also established that «synthetic diamond» is to be considered as real «diamond», thus allowing the synthetic stone producers to market their products as «real» / «true» diamonds.

The rest of the world and the international ISO standards foresee that, for the purposes of clarity and the consumers’ benefit, this gemmological material should only be called “synthetic diamond” the same as any other type of synthetic product. No other definition or simplification is allowed. ISO 18323:2015

The cost of this material is currently 30-40% lower than natural stone but further reductions are foreseen due to its ever-greater distribution and a reduction in production costs.

Synthetic diamonds currently represent about 2% of the global market. It is expected that, by 2030, this share will have risen to 10%. For stones that weigh around 0.50-1.50 ct, suitable to be used as solitaires, that is, for engagement rings, a 7.5% share could already be reached in 2020.

The share could reach 15% in the next two years for «melee».

The distribution of this material in melee could be intensified by a progressive scarcity of diamonds extracted from mines, since the Argyle mine, which currently supplies the majority of the world’s small diamonds, is soon to be closed (almost totally exhausted).

It is therefore difficult at this moment in time to predict exactly how this material will affect the jewellery market.

From marketing studies, it would seem that new generations are positively in favour of using this new material in personal ornamentation.

The diamond is losing its appeal as a symbol of rarity and eternal love and is becoming a highly common gem. Consumers are beginning to see synthetic diamonds as desirable: they can have much larger gems at lower prices and, above all, make an investment «without feeling guilty». Considerable media campaigns to publicize these gems as much more ‘ethical’ than their natural counterparts, are underway. The younger generations, rightly oriented towards the environment and the non-exploitation of natural and, above all, human resources, are showing greater interest in this type of gem compared to past generations, who were more greatly concerned about the uniqueness and rarity of each jewellery item.

Big names from the entertainment and web worlds, such as Di Caprio, Lady Gaga, Penelope Cruz or the owners of Facebook, Twitter and eBay, have publicized or even financed synthetic diamond production facilities, believing in their future. The Diamond Foundry, one of the latest US producers to appear on the market, has declared itself as the only producer currently supplying certified «carbon neutral» diamonds, since its stones are made in a hydroelectrically-powered plasma reactor. The company claims that: “mine extraction has a greater impact on the environment than any other human activity. For every single carat of diamond mined, about 250 tons of earth must be excavated and this releases a considerable amount of atmospheric pollution with heavy carbon dioxide emissions.”

Through its LIGHTBOX brand, De Beers has started the on-line sale of a line of colourless, blue and pink synthetic diamond jewellery at a much lower cost, trying to secure a significant share of the global market (1.00 ct 800.00 US$ – 0.50 ct 400.00 US$ – 0.25 ct 250.00 US$).

More than 60% of those interviewed in studies would be willing to buy, or interested in buying, a synthetic diamond for an engagement ring due to the lower cost of the material which would allow them to have a larger stone at a lower cost.

Consumers with financial resources, traditionally more bound to the charm and mysticism of the unique and unrepeatable … now seem to be showing a lot of interest in this material.

Synthetic diamond producers have been able to arouse the interest of the so-called «millennials» by promoting Lab Grown Diamonds as high-tech, innovative and clean.

In every aspect of their lives, Millennials look for brands, companies and products that they believe to be transparent, social and respectful of the environment.

Nowadays, consumers no longer believe in the value of diamonds or of jewellery in general. In fact, several factors have spread mistrust in the sector over the years.

Traders that lack transparency

Traders with a poor knowledge of the materials and market

Poor investment yield on diamonds

Few certainties

We must, however, bear in mind that: a natural diamond, even if poor in quality, will always have a potential buyer. There is, on the other hand, no secondary market for synthetic diamonds, especially since diamond traders currently tend not to deal in them. The «good bargain» aspect, or rather, the savings made on buying a synthetic diamond, becomes less tangible when you consider the fact that it will not be possible to re-sell it.

At the moment, the outlook is decidedly confusing and unclear. World traders, given the economic interest that rotates around the natural material, are decidedly concerned and scared about the sudden distribution and by the number of media campaigns that feature synthetic diamond.

But, if we look at the past what is happening now was promoted in exactly the same way before when, at the beginning of the last century, DeBeers, through targeted media campaigns and movie stars (we could mention Marylin Monroe and phrases like «diamonds are a girl’s best friend» and «diamonds are forever»), disseminated the use of diamonds in jewellery so that they could become a «symbol of true and eternal love» for everyone.

It is therefore hard to answer the initial question but perhaps we could now pose another: “could synthetic diamond be an opportunity?”

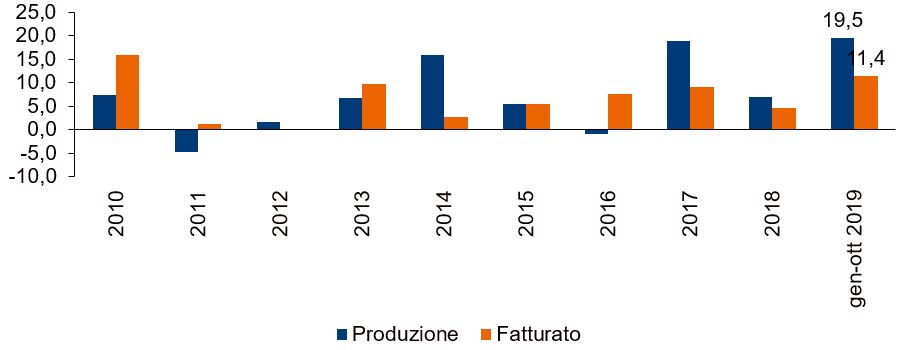

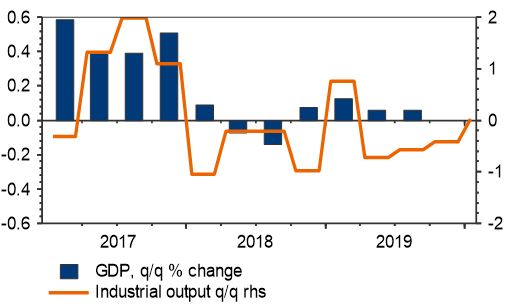

Secondo i dati ISTAT la produzione del settore gioielleria e bigiotteria ha registrato nei primi 10 mesi del 2019 una nuova forte crescita: +19,5%, per il terzo anno consecutivo.

In forte aumento anche il fatturato: +11,4% tra gennaio e ottobre 2019. Il fatturato è in crescita per il decimo anno consecutivo.

Evoluzione del fatturato e della produzione del settore orafo (var.%)

Settore orafo: codice ATECO 32.1 *2018: gennaio – novembre Fonte: Intesa Sanpaolo, elaborazioni su dati Istat

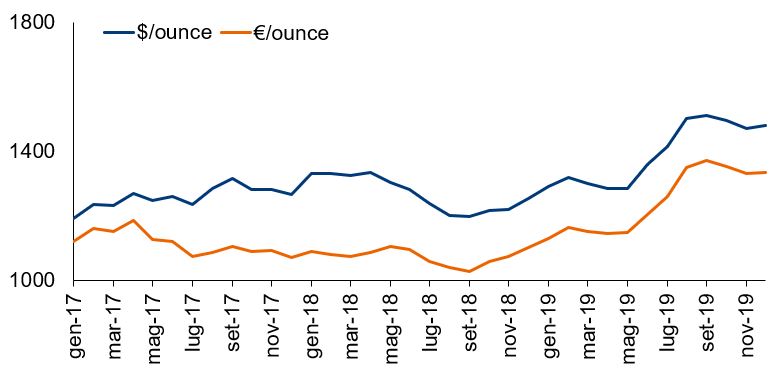

Prezzo dell’oro in crescita…

A partire dal mese di maggio la forte incertezza nello scenario globale ha comportato una significativa crescita del prezzo dell’oro che ha superato rapidamente i 1500 dollari oncia tra agosto e settembre per poi posizionarsi su livelli superiori alla media del 2018. Nella media del 2019 il prezzo dell’oro è aumentato del 15,9% in euro e del 9,7% in dollari.

Quotazioni mensili dell’oro

Fonte: elab. Intesa Sanpaolo su dati LME

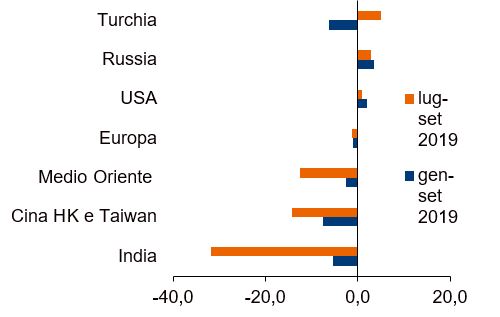

…con effetti negativi sulla domanda mondiale

La domanda mondiale di gioielli in oro ha reagito rapidamente al nuovo quadro dei prezzi, registrando una significativa contrazione nel terzo trimestre (-15,6%), in particolare sui due principali mercati (Cina e India) ed in Medio Oriente.

Domanda mondiale di gioielli in oro: var.% tendenziali (tonnellate)

Domanda mondiale di gioielli in oro: var.% tendenziali per paese

Fonte: Intesa Sanpaolo sudati World Gold Council – Gold Demand Trends

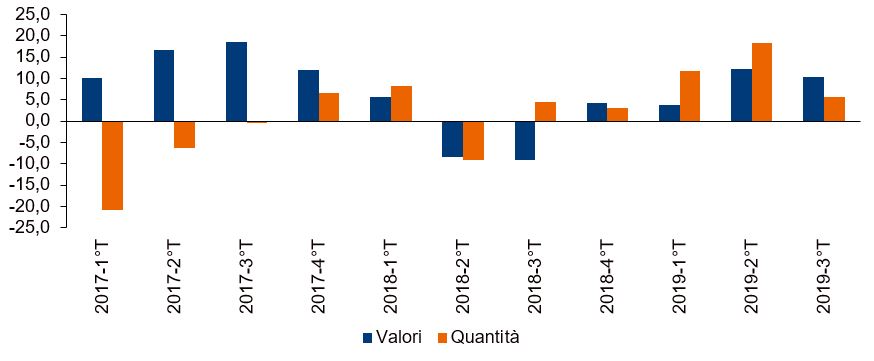

Ottime performance per l’export italiano…

Nei primi nove mesi del 2019, le esportazioni di gioielli in oro sono cresciute del 12,1% in quantità e dell’8,8% in valore in euro.

Evoluzione delle esportazioni di gioielli in oro (var.% tendenziale)

* Codici HS 711319 per oro e altri preziosi Fonte: Intesa Sanpaolo, elaborazioni su dati Istat

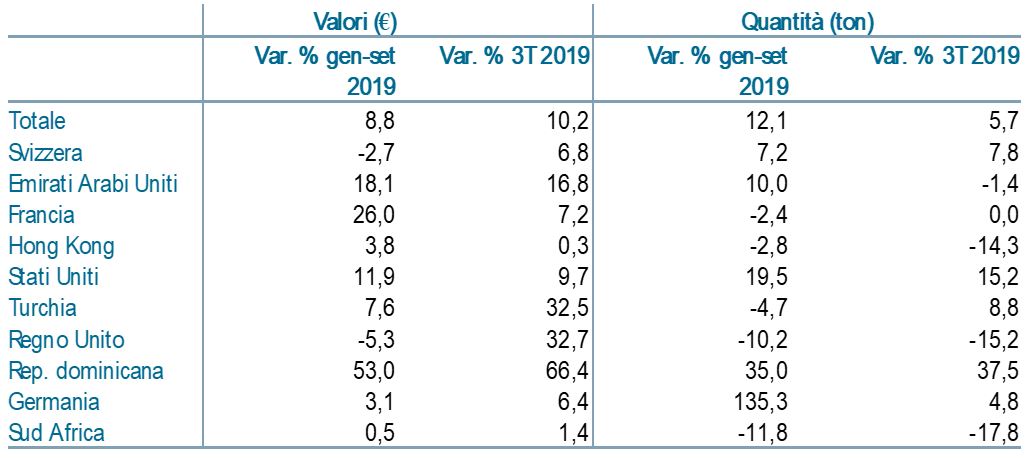

…con risultati positivi diffusi a (quasi) tutti i mercati…

Evoluzione delle esportazioni italiane di gioielli in oro (var.% tendenziale)

* Codici HS 711319 per oro e altri preziosi Fonte: Intesa Sanpaolo, elaborazioni su dati Istat

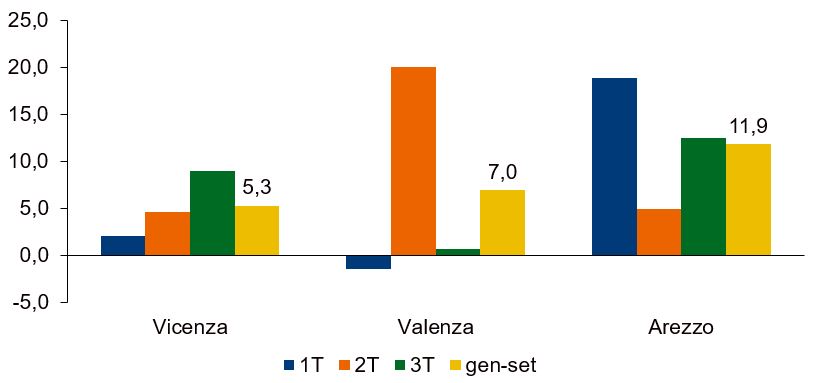

…e i distretti

Le esportazioni provinciali sono disponibili solo a livello più aggregato (inclusa la bigiotteria) e solo in valore (e non in quantità). Tutti i territori hanno registrato una evoluzione positiva, con risultati più brillanti per Arezzo.

.

Esportazioni italiane di gioielli e bigiotteria* nel 2019 (var.%)

*Codice 32.1 Fonte: elab. su dati ISTAT

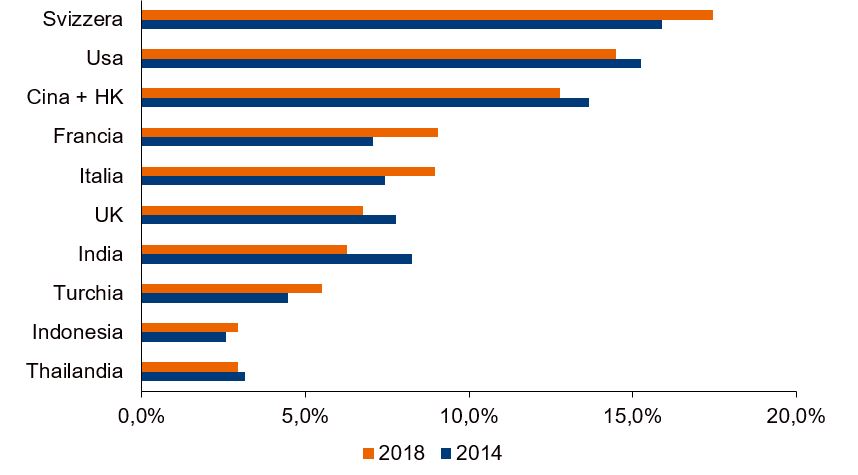

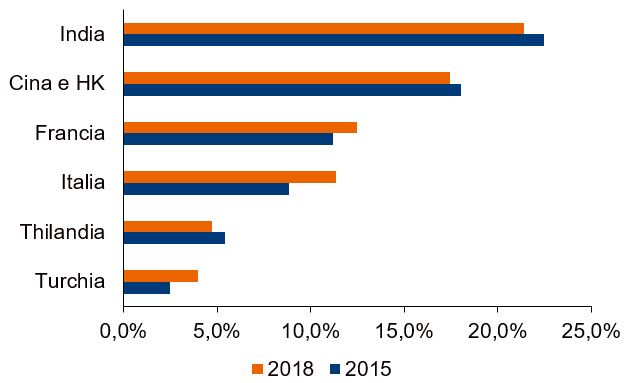

Il successo del lusso traina Svizzera, Francia e Italia

Quote sulle esportazioni mondiali di gioielli in oro* (%) N.B. Al netto dei flussi verso e dagli Emirati Arabi Uniti e tra Cina e Hong Kong *Codice 711319 Fonte: elab. su dati UNCTAD Comtrade

Ottimi risultati negli USA

Quote sulle importazioni USA di gioielli in oro* (%) *Codice 711319 Fonte: elab. su dati US Trade

Le prospettive per i prossimi mesi

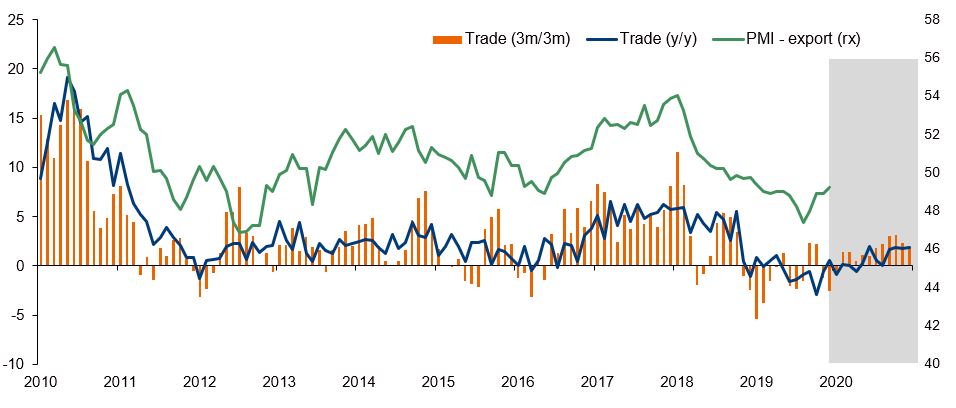

Commercio mondiale in ripresa, ma trend di crescita modesto

Le variazioni sono calcolate sull’indice mensile di commercio mondiale CPB. L’area ombreggiata indica le proiezioni. Fonte: elaborazioni Intesa Sanpaolo

Le previsioni al 2021

Lieve ripresa nel primo semestre 2020 ma dato annuo inferiore al 2019 a causa di un effetto trascinamento penalizzante.

Attesa una leggera accelerazione (dei dati annui) nel 2021, anche grazie agli accordi sul commercio.

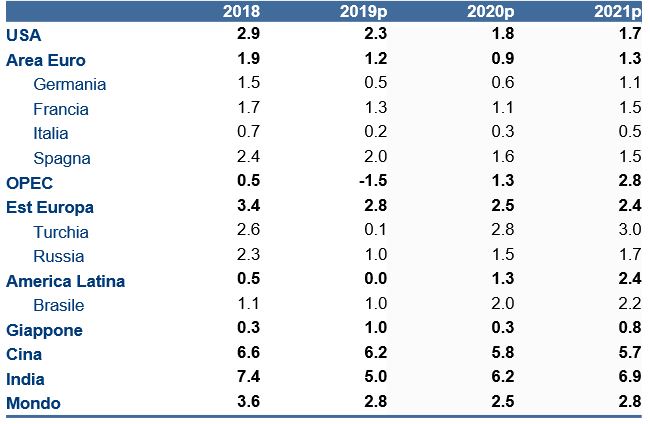

Le previsioni di crescita del PIL

Fonte: Refinitiv-Datastream ed elaborazioni Intesa Sanpaolo

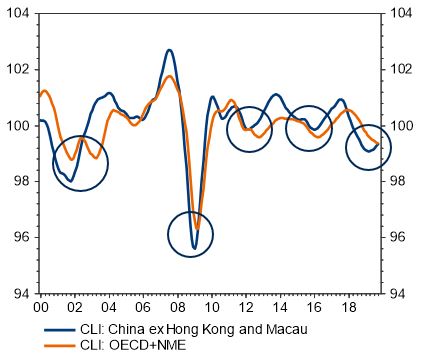

Dall’Asia i primi segni di stabilizzazione del ciclo

L’indice anticipatore OCSE per la Cina conferma la svolta

Fonte: OECD

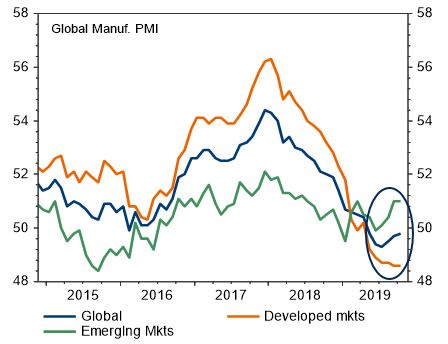

PMI manifatturiero Globale beneficia della ripresa dei Paesi emergenti

Fonte: IHS Markit

Ciclo USA: rallentamento controllato

Crescita verso il potenziale

Fonte: Refinitiv-Datastream

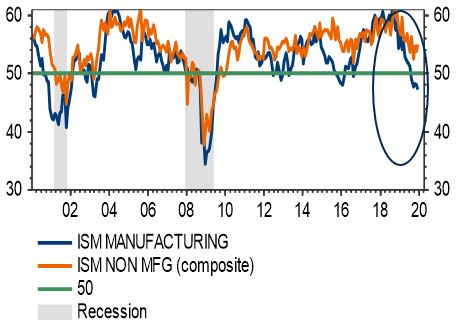

Manifatturiero in via di stabilizzazione

Fonte: Refinitiv-Datastream

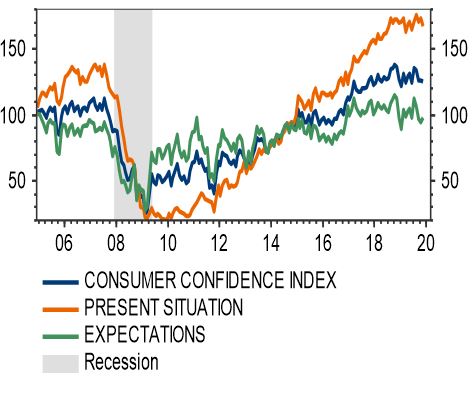

I consumatori sono ottimisti

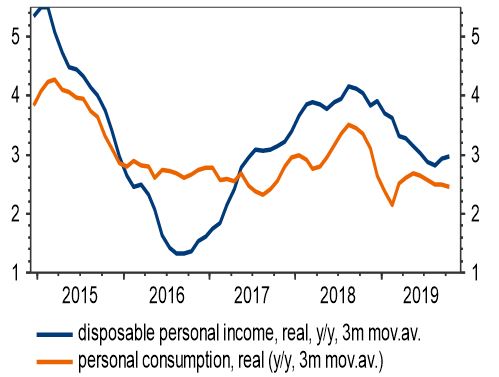

Crescita dei consumi sostenuta da una dinamica solida del reddito disponibile

Fonte: Refinitiv Datastream

Le famiglie sono molto ottimiste

Fonte: Refinitiv Datastream

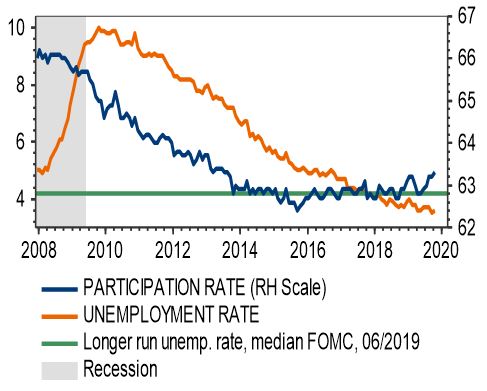

Il mercato del lavoro è la forza trainante dei consumi: disoccupazione sui minimi dal 1969

Il tasso di disoccupazione è sui minimi da fine 1969…

Fonte: Refinitiv Datastream

…con la dinamica salariale in accelerazione

Fonte: Refinitiv Datastream

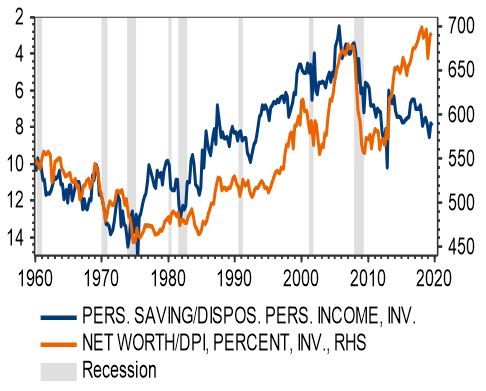

I bilanci delle famiglie sono finalmente in ordine

Ricchezza netta in continuo aumento e tasso di risparmio sui livelli degli anni ‘90

Fonte: Refinitiv Datastream

Le famiglie hanno ridotto il loro debito, le imprese e il settore pubblico no

Fonte: Refinitiv Datastream

Area euro: domanda interna sostenuta da redditi reali e politiche fiscali

Crescita salariale e occupazione sostengono redditi e consumi

Fonte: Eurostat e proiezioni Intesa Sanpaolo

Saldo primario corretto per il ciclo: i budget 2020 mostrano un modesto allentamento (0,3% a livello di Eurozona)

Fonte: Commissione Europea

Domanda estera più favorevole nel 2020

Per l’area euro la domanda estera dovrebbe riprendersi parzialmente nei prossimi trimestri

Fonte: stime Intesa Sanpaolo e Oxford Economics

Italia: crescita ancora modesta

Per il 2020 ci aspettiamo una lieveaccelerazione a 0,3% (0,4% non corretto per i giorni lavorativi), dallo 0,2% del 2019.

Attesa una crescita dello 0,5% nel 2021.

Il PIL è cresciuto negli ultimi trimestri nonostante una contrazione dell’attività industriale

Fonte: Refinitiv-Datastream, Istat ed elaborazioni Intesa Sanpaolo

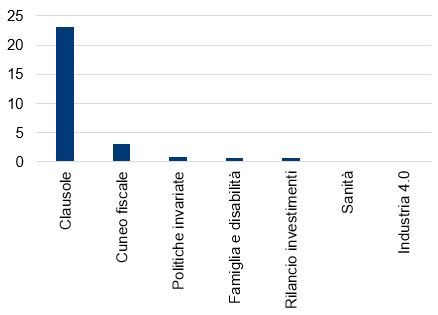

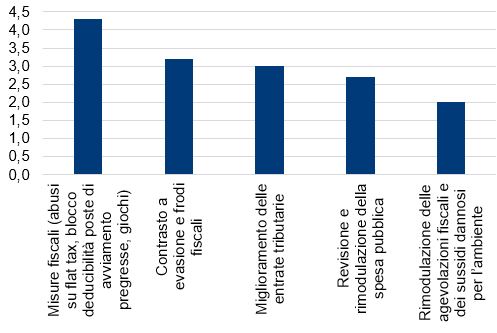

Legge di bilancio: risorse destinate al blocco dell’IVA

Le modifiche dell’ultim’ora hanno visto un alleggerimento e un rinvio a luglio della plastic tax, uno slittamento a ottobre della sugar tax e un sostanziale azzeramento della stretta sulle auto aziendali. La manovra è salita a 32 miliardi.

Interventi (impatto in miliardi sul 2020)

Coperture (impatto in miliardi sul 2020)

Nota: effetto sull’indebitamento netto in miliardi Fonte: elaborazioni Intesa Sanpaolo su DPB 2020

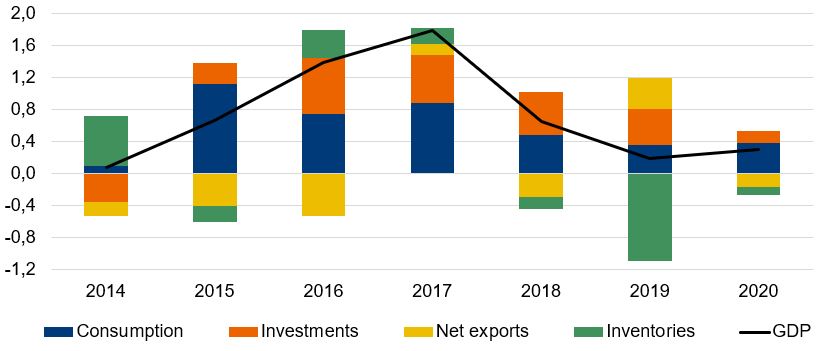

Tenuta dei consumi grazie ad una buona dinamica del reddito disponibile

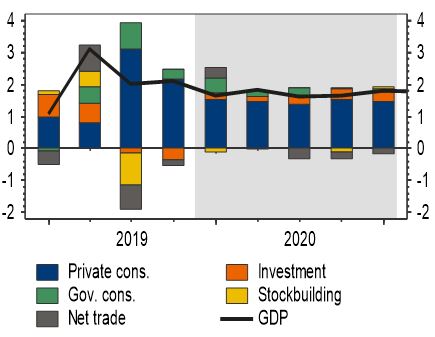

Contributi alla crescita delle varie componenti del PIL

Fonte: Refinitiv-Datastream, Istat ed elaborazioni Intesa Sanpaolo

Un ritorno alla crescita è possibile nel medio termine

Il calo dei tassi di interesse comporta, oltre a risparmi per lo Stato, anche una spinta alla crescita del PIL

La ri-accelerazione degli aggregati monetari (la cui svolta ha sempre anticipato quella del ciclo) fa sperare in un ritorno alla rescita del PIL nel medio termine

Nota: effetti cumulati di un calo di 100 punti-base dei rendimenti sui titoli di Stato a medio e lungo termine (circa in linea con quello registrato negli ultimi 6 mesi) sul PIL (deviazioni % rispetto al baseline) e sulla spesa per interessi della PA (in % del PIL).

L’incertezza geopolitica dovrebbe continuare anche nel 2020 a sostenere il prezzo dell’oro che nelle nostre attese dovrebbe proseguire il percorso di consolidamento, rimanendo nella media del 2020 intorno ai 1500$/oncia troy, con potenziali rischi al rialzo derivanti dall’ampia liquidità sui mercati e da politiche monetarie espansive in tutte le aree.

Prezzo dell’oro ($/oncia troy) Fonte: elab. su dati LME

Euro in lieve apprezzamento su USD in un orizzonte di 12 mesi

Fonte: Intesa Sanpaolo

Importanti comunicazioni

Gli economisti che hanno redatto il presente documento dichiarano che le opinioni, previsioni o stime contenute nel documento stesso sono il risultato di un autonomo e soggettivo apprezzamento dei dati, degli elementi e delle informazioni acquisite e che nessuna parte del proprio compenso è stata, è o sarà, direttamente o indirettamente, collegata alle opinioni espresse.

La presente pubblicazione è stata redatta da Intesa Sanpaolo S.p.A. Le informazioni qui contenute sono state ricavate da fonti ritenute da Intesa Sanpaolo S.p.A. affidabili, ma non sono necessariamente complete, e l’accuratezza delle stesse non può essere in alcun modo garantita. La presente pubblicazione viene a Voi fornita per meri fini di informazione ed illustrazione, ed a titolo meramente indicativo, non costituendo pertanto la stessa in alcun modo una proposta di conclusione di contratto o una sollecitazione all’acquisto o alla vendita di qualsiasi strumento finanziario. Il documento può essere riprodotto in tutto o in parte solo citando il nome Intesa Sanpaolo S.p.A.

La presente pubblicazione non si propone di sostituire il giudizio personale dei soggetti ai quali si rivolge. Intesa Sanpaolo S.p.A. e le rispettive controllate e/o qualsiasi altro soggetto ad esse collegato hanno la facoltà di agire in base a/ovvero di servirsi di qualsiasi materiale sopra esposto e/o di qualsiasi informazione a cui tale materiale si ispira prima che lo stesso venga pubblicato e messo a disposizione della clientela.

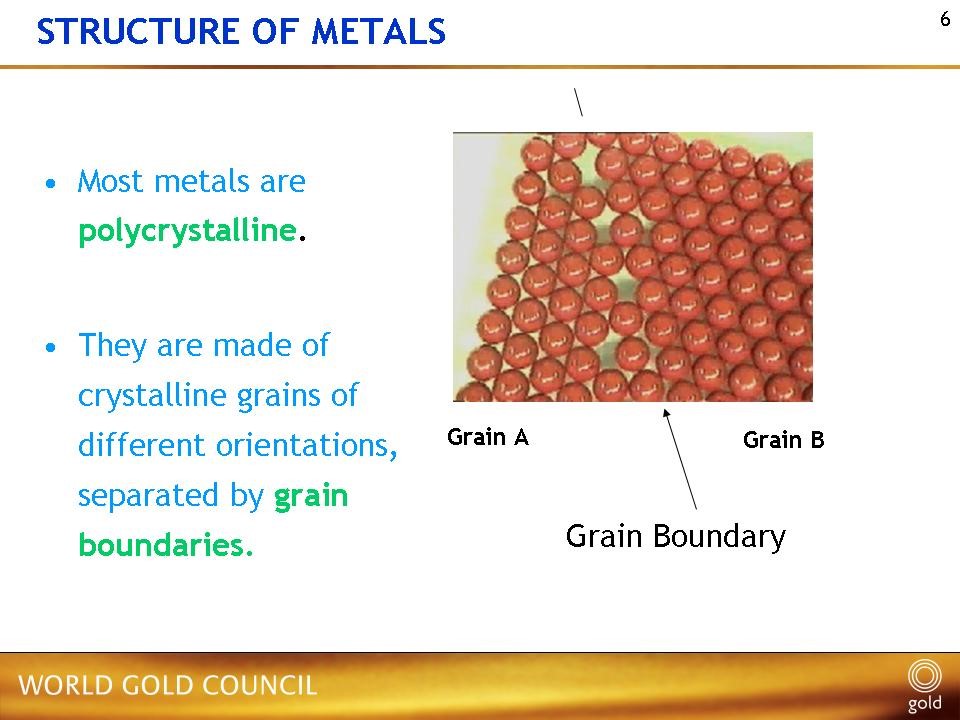

The importance of grain size in jewelry alloys and its control

a speech by Chris Corti

Abstract

Control of grain (crystal) size in jewellery manufacture is important for several reasons. It affects the properties of the alloys – mechanical, chemical and physical. These, in turn, influence the manufacturing process and the jewellery’s behaviour during wear by the customer. There are a number of ways grain size (and shape) can be controlled in precious metal jewellery alloys – by casting, working and annealing and by use of alloying additives that refine the grain size during casting and during working and annealing. These are reviewed and discussed in terms of their mechanisms, ease of use and their effectiveness. Some of the problems that can arise from lack of control will also be discussed. The focus of the presentation will be on gold alloys but all precious metals are considered.

Introduction

Anyone involved in the making of jewellery should have an appreciation of the nature of the metals and alloys with which they work and understand how alloying and processing of the metals influences the microstructure and consequently their properties. For jewellery, we focus on the alloys of the precious metals – gold, silver, platinum and palladium, all four of which are inherently ductile metals – but what I say is of general validity and applies to most metals.

Two fundamental points to understand are that1:

Alloy composition, microstructure and processing history are interrelated, Figure 1, and jointly influence an alloy’s properties, be they chemical (e.g. corrosion and tarnish resistance), physical (e.g. density, colour) or mechanical (e.g. strength, malleability, hardness). These, in turn, influence manufacturability and service performance.

Most metals and alloys are composed of many crystals, or grains as we metallurgists call them; thus, most alloys are polycrystalline. There are some rare exceptions such as single crystal aero turbine blades and amorphous or glassy metals.

In this presentation, I want to focus on alloy macro- and micro-structures, particularly grain size and shape. How we can influence them by casting, alloying and by mechanical working and annealing? Why are they important?

Figure 1 – Interrelationship of alloy composition, microstructure and processing history on properties (schematic)

Importance of grain size to jewelry

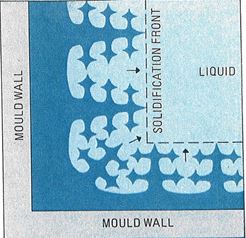

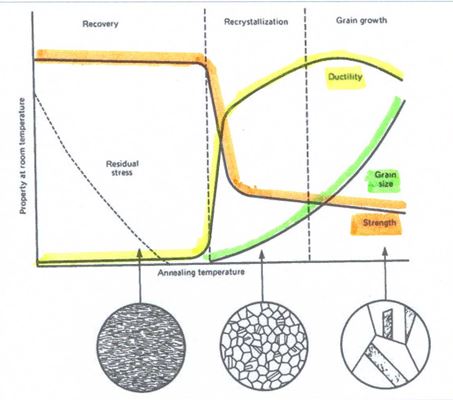

As jewellers attending this Jewellery Technology Forum will know, metallurgists pay some attention to the crystal, or grain, size in their alloys. We talk about ‘large (or coarse) grains’ or small (or fine) grain sizes and generally state the desirability of the latter in terms of jewellery production. The terms ‘large’ and ‘small’ are, of course, relative. But for practical purposes, ‘Large’ will usually mean grains of the order of millimetres or larger and ‘small’ will refer to grain sizes of the order of tenths or hundredths of a millimetre (1 – 100 microns). You may also hear of grain sizes referred to in terms of an ASTM numerical value. This is a comparative method of measuring grain size. The higher the number, the smaller is the grain size.

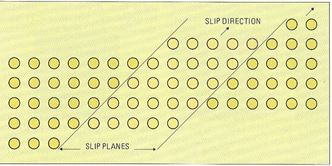

Why is control of grain size (and shape) important? Well, it is down to the relation between the grains (crystals) and the grain boundaries – the region at the junction of adjacent grains – and their relative influence on mechanical deformation processes. Grain boundaries are where the atoms sitting on the crystal lattices of adjacent grains do not match across together, creating a narrow region of imperfect crystal, Figure 2. Often, these can be a preferred site for deleterious impurities and second phases, leading to embrittlement. At low or ambient temperatures, the deformation process under an imposed load is governed mainly by the dislocation slip mechanism within each grain (dislocations are linear crystal defects responsible for deformation on crystal slip planes). Without going into deep explanations, the outcome is that alloys with finer grains are stronger than those with large grains, and this effect is expressed by the Hall-Petch relationship in which yield strength, σy.s., is inversely related to the grain size squared:

σy.s. = m/d2

where d is the average grain diameter and m is a constant. The yield strength of a material (known also as the Elastic Limit or proof stress) is the stress required to start plastic deformation and is smaller than the ultimate tensile strength (‘UTS’).

Thus, the jewellery is stronger and harder if it is fine-grained and, beneficially, it is also more ductile and less prone to cracking, impurity embrittlement and the ‘orange peel’ surface after deformation. As jewellery is generally only subject to relatively simple stresses (loads) at ambient temperatures, whether in a production environment or in service, a fine grain size is therefore desirable. This is generally true for other non-precious engineering components such as sheet steel for car bodies and white goods.

Figure 2 – Schematic of a grain boundary, showing the mismatch of crystal structure at the boundary

On the other hand, engineering components can be subjected to often-complex stresses over long periods at high temperatures; for example, turbine blades and disks in jet engines and boiler tubes in utility power stations. At these high temperatures, the main deformation mechanisms are phenomena such as creep and fatigue. Creep is the slow deformation under a steady low stress or load and fatigue is the mechanical failure under an alternating load. The lead sealing on a tiled church roof is actually at a hot working temperature and so slowly creeps under its own weight. Under such conditions, the grain boundaries are weaker and grains can slide over each other; hence, a large grain size is preferred as there is relatively less grain boundary area. In the ultimate, such as gas turbine blades, we prefer to eliminate grain boundaries, so we find use of directionally solidified alloys and even single crystal alloys for optimum creep and fatigue strength. An extreme of fine grain sizes is a phenomenon known as superplastic deformation, whereby alloys with stable, fine grain sizes can be gently deformed at temperature under low stresses to very large deformations, just like Swiss cheese fondue. Several titanium aircraft components of complex shape are manufactured by this technique including the very large fan blades on Rolls Royce jet engines. Interestingly, fine-grained sterling silver can be superplastically deformed under the right conditions2 and I would expect some other precious metal alloys also to do likewise. But to date, that ability has not been developed or commercially exploited in our industry.

Examination of microstructure: metallography

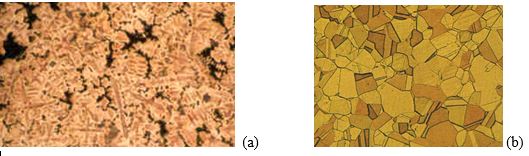

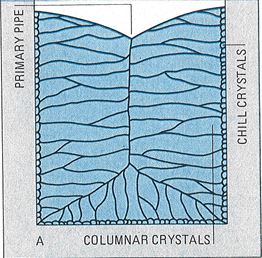

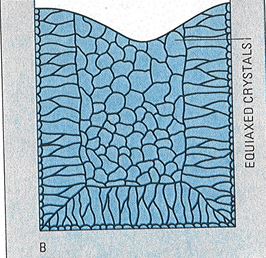

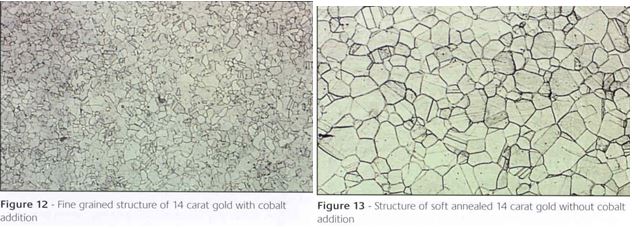

As many of you will also know, we can examine the microstructure and measure the grain size of a piece of jewellery metal; due to the scale of this, it is often performed under an optical microscope. The process of examining grain size and general microstructure is called ‘metallography’. Figure 3 shows the microstructure of both as-cast and cold worked and recrystallized gold alloys. There are obvious differences in appearance and these will be explained later.

Figure 3 – Microstructure of typical karat gold alloys (a) as cast, (b) worked and annealed

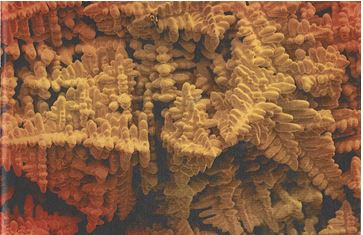

Normally, if we wish to examine the macrostructure or microstructures of an alloy, we need a flat polished surface as optical microscopes have a limited depth of focus. In order to expose the features such as grain boundaries and second phases, we often need to etch the surface with a corrosive liquid such as acid. As grain boundaries are less perfect than the crystals, they etch preferentially to reveal themselves. As different crystals are oriented in different directions relative to the plane of the surface, they also etch at different rates and so appear of different contrast or colour to the eye. Where more than one phase is present, these also etch differently and usually show themselves as different colours or shades of darkness.

If we need greater magnification than we can get in an optical microscope to see the features of interest or we have an uneven surface such as a fracture, then we use a scanning electron microscope. Here flatness of the surface is not such an issue as in optical light microscopy and we can often see different phases by atomic number contrast, without the need for etching (see figure 22 in reference 3, for example)3,4. The heavier elements appear whiter under the SEM and the lighter ones darker, so giving rise to differences in contrast with varying alloy phase composition.

Casting